Transportation and Capacity

Firm vs interruptible transportation, the secondary market for pipeline capacity, capacity release, and the contractual layer that sits over the physical pipe.

On Tue Jan 7, 2014, PJM Interconnection’s 13-state footprint pulled 141,846 megawatts at the morning peak, a winter record at the time. Air temperatures held below 5 degrees Fahrenheit across Newark, Pittsburgh, and Columbus through the morning. Gas-fired generation made up nearly half of PJM’s installed capacity. On a normal cold day those units would have provided most of the marginal energy. On this morning they did not.

Forced and unplanned outages across PJM hit roughly 40,200 MW, a system-wide forced outage rate above 22 percent against the typical 7 percent. Gas-fired units were the largest share of the outage stack. The unit-level causes ran across frozen instrumentation and air intakes, mechanical trips on units that had been started cold after months of standby, and fuel-supply interruptions. The fuel-supply interruptions traced directly to the contract layer this chapter unpacks.

Tennessee Gas Pipeline, Texas Eastern Transmission, and Transco each declared Critical Day Operational Flow Orders during the polar vortex week, curtailing volumes to shippers without firm primary point-to-point capacity. Power generators that had nominated under interruptible service or that held capacity-release positions junior to LDC recall rights had their nominations cut. The pipelines were physically full of gas. The contracts said the gas was not theirs to take.

The polar vortex week ended with PJM clearing several hundred million dollars of January uplift charges against load-serving entities for the cost of out-of-merit dispatch and emergency capacity, with the full multi-month polar vortex uplift exceeding $1 billion across the winter. The chapter that follows is the contract architecture that determined which generators ran on Tue Jan 7, 2014, and which sat on the sidelines while the lights stayed on.

Firm vs Interruptible Transportation: The Service Tiers

Firm Transportation is the primary commercial contract for moving gas on a US interstate pipeline. The shipper holds a contract with the pipeline that specifies a Maximum Daily Quantity, the maximum volume the shipper has the right to nominate on any gas day, expressed in thousand decatherms per day or in MMBtu per day. The shipper pays a monthly reservation charge, called the demand charge, on that MDQ. The reservation charge is paid every month regardless of whether the shipper actually nominates any gas. A small per-MMBtu usage charge, called the commodity charge, is paid only on the volume that physically moves. The combined demand-plus-commodity rate is the all-in unit cost of FT service when capacity is fully utilized; the demand-only rate is the cost when the capacity sits idle.

Firm Transportation contracts run from one year to twenty-five years. A new pipeline construction project requires precedent agreements with shippers covering 50 to 70 percent of the project’s design capacity at 15 to 25 year tenors before FERC will issue a Section 7 certificate, the regulatory predicate covered in Chapter 10. The long-tenor demand-charge stack is the cash flow that underwrites the project debt and equity. Shippers signing those contracts are the financial counter-parties that make a 42-inch mainline buildable.

The shipper’s primary point-to-point right under a firm contract is the contractual specification of the receipt point on the pipeline (where the shipper delivers gas in) and the delivery point (where the shipper takes gas out). FT shippers have priority over all other classes of service when nominating between their primary points. A shipper nominating from a non-primary receipt point or to a non-primary delivery point falls into a secondary firm class, with priority above interruptible service but below the holders of primary point-to-point rights at the contested nodes.

Interruptible Transportation carries no daily guarantee. The IT shipper pays a per-MMBtu usage charge on the volume actually moved with no reservation charge and no demand charge. The pipeline accepts IT nominations only if firm shippers have not nominated their full contracted capacity at the relevant points. On a constrained day, IT is curtailed first. The IT shipper has the cheapest tariff rate on a normal day and the least reliable molecule on a peak day. The asymmetric service is the right service for shippers whose own load is itself interruptible, including some industrial process loads, opportunity buyers in the daily market, and gas-fired peaker units that operate only on the warmer 200 days of the year.

Several intermediate service classes layer in between firm and interruptible. Secondary firm is firm capacity that the pipeline can move outside the holder’s primary points subject to availability. No-notice service is a premium FT variant available on selected pipelines, typically priced at a premium to standard FT, that allows the shipper to change nominations intraday without prior commitment; LDCs serving high-swing residential heating loads are the primary no-notice buyers. Storage service, addressed in Chapter 11, bundles firm injection capacity, firm withdrawal capacity, and firm working-gas capacity into a single tariffed product. Park-and-loan service permits an operator to temporarily place gas with the pipeline (a park) or borrow gas from the pipeline (a loan), with the rate set as an option-style premium and the volume used for short-term operational balancing.

The firm-capacity book on a major US pipeline in 2024 distributes across five commercial buyer classes. Local distribution companies hold the largest single share by reserved MDQ, with the residential and small-commercial winter peak driving demand-charge commitments that span the lifetime of the underlying utility franchise. LNG export terminals are the fastest-growing FT segment since the December 2015 statutory lifting of the US crude oil export ban and the start-up of Sabine Pass Train 1 in early 2016. Gas-fired power generators concentrated in PJM, MISO, and ERCOT are the third major segment, with the firm-versus-interruptible mix on the generator’s contract book setting whether the unit is dispatchable on a critical day. Large industrial end-users (chemicals, fertilizer, steel, glass) are the fourth, holding firm capacity sized to plant turnaround schedules and to long-term offtake contracts. Producers and marketers contracting transport from origin hubs to demand hubs hold the fifth, with the marketer book as the source of much of the capacity release flow that the next section addresses. The firm-capacity book is the contractual permission slip for the molecule on a peak day.

The Capacity Release Secondary Market

FERC Order 636, issued on Wed Apr 8, 1992, created the firm shipper’s right to resell unused contracted capacity. Before Order 636 the pipeline operated as the bundled merchant, holding both the gas and the transport, and the LDC bought a delivered product. After Order 636 the LDC held the firm transport contract directly with the pipeline and could resell some or all of its contracted MDQ when its own demand fell short. The capacity release market is the secondary market in which that resale happens.

Three transaction structures dominate. The pre-arranged release is a privately negotiated transaction between a releasing shipper and a replacement shipper; the parties agree on volume, term, points, and rate, and the pipeline confirms the transaction against the underlying contract. Pre-arranged releases handle the bulk of long-term and seasonal capacity reallocations. The posted release is a public posting on the pipeline’s electronic bulletin board with specified terms (volume, term, points, minimum release rate); other shippers bid against the posting in an electronic auction window, typically running for a defined number of hours under the pipeline’s tariff. Posted releases handle the bulk of monthly bidweek capacity reallocation, with most major US pipelines running their bidweek auctions in the four business days that precede the Inside FERC publication date covered in Chapter 15. The one-shot release is a single-day or two-day release for operational balancing, typically posted intraday as shippers identify excess capacity.

The pricing structure connects capacity release to the underlying tariff. The release rate, the payment from the replacement shipper to the releasing shipper, is generally capped at the pipeline’s tariff-specified maximum reservation rate for the same point-to-point service, called the recourse rate. FERC Order 712, issued on Thu June 19, 2008, removed that cap on short-term capacity releases of one year or less, recognizing that the cap was preventing the market from pricing scarcity on tight days. Long-term releases over one year remain subject to the recourse-rate cap. The Order 712 reform unlocked the bidweek and daily capacity release auction as the visible price screen for locational scarcity of pipeline capacity. Algonquin Gas Transmission posted release rates above $50 per MMBtu in January 2018 during the bomb cyclone and again above $20 per MMBtu in December 2022 during Winter Storm Elliott; both were the bidweek auction prints that anchored the corresponding cash basis at Algonquin Citygate.

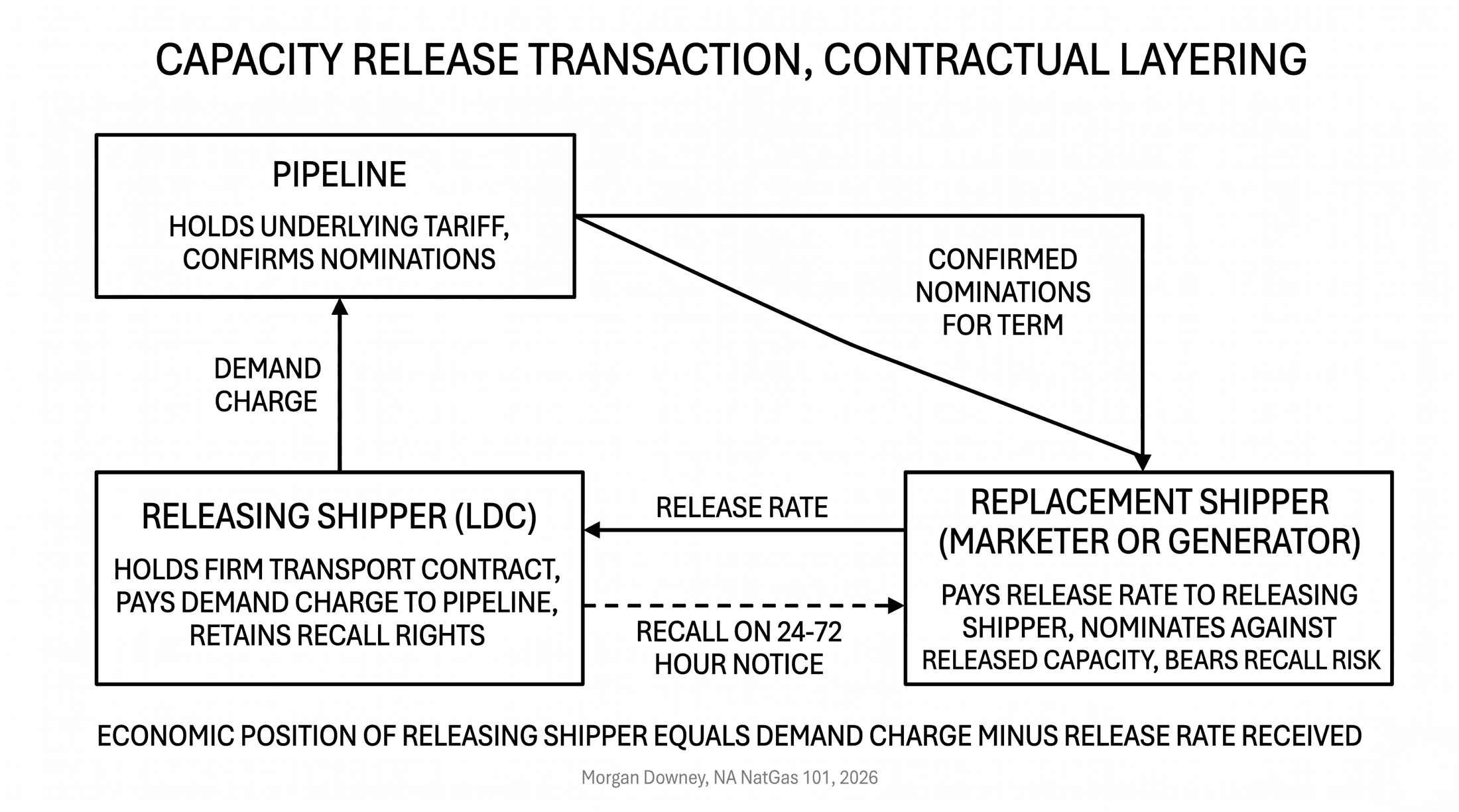

The contractual relationships under a capacity release transaction are layered. The releasing shipper retains the underlying firm contract with the pipeline and continues to pay the demand charge. The replacement shipper pays the release rate to the releasing shipper, who in turn pays the demand charge to the pipeline. The pipeline confirms the transaction and processes the replacement shipper’s nominations as if the replacement were the holder of the underlying capacity for the duration of the release. The releasing shipper’s economic position is the demand charge minus the release rate received; in tight markets that figure is negative, meaning the releasing shipper makes a profit on the release; in slack markets that figure is positive, meaning the releasing shipper carries the cost of unused capacity.

The economic logic of the structure is that the LDC is obligated by state regulation to maintain firm capacity sized to its design day, the peak winter day used for resource adequacy planning. A typical Northeast LDC sizes firm capacity to a winter day with a 1-in-30-year severity, meaning the LDC’s contracted firm capacity exceeds its average winter sendout by a substantial margin. The unused fraction of that capacity has commercial value to a power generator, a marketer, or an industrial buyer who would otherwise have to procure interruptible transport with no priority. The capacity release market converts the LDC’s regulatory-driven over-procurement into revenue, with the proceeds either flowing back to the LDC’s ratepayers through cost-of-service adjustment mechanisms or accruing to the marketer that runs the LDC’s portfolio under an asset management agreement.

The visible bulletin-board posting is the price discovery signal. Each major US pipeline publishes its capacity release postings on a public electronic bulletin board with each posting tagged by volume, term, primary and secondary points, recall rights, and current bid. The posting set across all major pipelines is read in aggregate by traders, hedgers, and infrastructure analysts as the cleanest available signal for which pipelines are full and which are not. A high posted release rate at a given point is the mirror image of a high basis at the same point. The capacity release market and the basis swap market price the same underlying scarcity, the first as a transport tariff, the second as a delivered-cost differential. The two prices anchor each other across the bidweek window.

Recall, Replacement Rights, and Contractual Flexibility

The releasing shipper typically retains recall rights, the contractual right to take back released capacity on specified notice if its own demand requires it. Recall is the LDC’s insurance against weather. A Boston-area LDC that releases 100,000 MMBtu/d of firm Tennessee Gas Pipeline capacity to a New England power marketer in October at a modest seasonal rate keeps the right to recall that capacity in January when a polar low pulls residential heating sendout above the LDC’s other firm-supply commitments. Recall provisions vary by pipeline tariff and by individual release contract; a typical structure on a Northeast LDC’s release allows recall on 24-to-72 hour notice with a defined number of permitted recall events per gas year.

The replacement shipper bears the recall risk. A power generator that takes a 6-month seasonal release with 24-hour recall has effectively bought firm transport with a contingent claim against it; the generator can dispatch on that capacity 99 percent of the time, but the 1 percent of the time the recall fires is the polar vortex morning when the generator most wants the gas. Pipelines distinguish between recallable and non-recallable releases in tariff postings. Non-recallable releases typically clear at materially higher rates than recallable releases for the same volume and term, because the replacement shipper has certain access for the duration. The price gap between recallable and non-recallable releases on a Northeast pipeline in a tight winter month can be a multiple of two times or more, reflecting the option value of the recall right.

Replacement rights run the other direction. If the replacement shipper defaults on the release rate or fails to nominate against the released capacity, the releasing shipper retains the right to re-nominate the capacity on its own behalf or to release the capacity again to a different replacement. The replacement-rights provisions protect the LDC against a counter-party default; the LDC’s residential customers do not freeze if the marketer holding the release goes bankrupt mid-winter. Pipeline tariffs require the releasing shipper to act on a default within a defined window, typically one to three gas days, after which the underlying capacity reverts to the pipeline’s standard interruptible queue.

The full structure is a layered set of contingent rights, with the LDC’s regulated obligation to serve its captive customers at the top of the stack. The LDC contracts firm primary capacity. The LDC retains recall rights against any release. The replacement shipper pays a discount to non-recallable rates in exchange for accepting the contingent claim. The replacement shipper protects against its own counter-party risk through replacement rights. The pipeline confirms each level of the stack against its tariff and processes the resulting nominations on each gas day.

The contractual flexibility is what makes the capacity release market viable as a commercial instrument. Without recall, the LDC would not release. Without replacement rights, the marketer would not pay for the release. Without the standardized tariff mechanics that govern both, the release would not clear at a transparent price.

Asset Management Agreements

Asset Management Agreements are bundled commercial arrangements under which a shipper outsources its gas supply, transport, and storage management to a marketer. The shipper, typically an LDC or a power generator with a substantial gas portfolio but no in-house gas-trading desk, retains the underlying firm transport and storage contracts with the pipeline and continues to pay the demand charges. The marketer takes operational control of the portfolio, schedules nominations on the pipeline through the NAESB cycles addressed in the next section, manages day-ahead and intraday balancing against the shipper’s load, and procures supply at the relevant origin hubs. The marketer captures any optimization upside from running the portfolio, including capacity release rates above the recourse cap on tight days, storage cycle profits, and basis arbitrage between origin and delivery hubs. In exchange the marketer pays the shipper a fixed annual fee, a profit-share on the optimization, or a combination structure.

The AMA is the most common path through which large LDCs participate in the capacity release market without operating an in-house gas-trading floor. A municipal or regulated investor-owned LDC with several hundred million dollars per year of gas procurement spend lacks the scale to staff a 24-hour trading desk, a NAESB nominations group, and a credit and counter-party operation. The AMA marketer runs those functions on behalf of multiple LDCs simultaneously and aggregates the optimization across the portfolio. The marketer’s incentive is to maximize the spread between the LDC’s demand-charge stack and the realized release-and-arbitrage revenue; the LDC’s incentive is to minimize the all-in delivered cost of gas to its captive customers, and the AMA fee structure attempts to align the two.

Major US AMA marketers in 2024 include BP Energy Company, Shell Energy North America, Macquarie Energy, Tenaska Marketing Ventures, and Sequent Energy Management (now part of Williams following the 2021 acquisition that absorbed Sequent into the Williams marketing platform), along with EDF Trading North America, Direct Energy Business Marketing (a subsidiary of NRG Energy), Symmetry Energy Solutions, and a handful of regional players.

The AMA structure is regulated under FERC’s Standards of Conduct, the affiliate-transaction rules originally codified in Order 497 (1988) and updated through Order 717 (2008) and subsequent amendments. The Standards of Conduct require that any release from an interstate pipeline or its affiliate to an affiliated marketer be posted publicly first on the pipeline’s electronic bulletin board, with non-discriminatory access for non-affiliated bidders. The rule prevents a pipeline-affiliated AMA marketer from taking favorable releases that would not have been offered to an arm’s-length competitor. Compliance is enforced through periodic FERC audits, posting-record reviews, and self-reporting by the pipeline operator.

The AMA layer is the operational bridge between the LDC’s regulated retail business and the wholesale gas trading market. The retail customer pays the delivered tariff. The marketer captures the margin on the optimization. The pipeline holds the underlying firm contract that anchors the entire structure.

NAESB Nomination Cycles and the Daily Flow Schedule

Pipeline gas flow is scheduled through five daily nomination cycles defined by the North American Energy Standards Board, the industry standards-setting body that has published the Wholesale Gas Quadrant Standards since the late 1990s. NAESB superseded the earlier Gas Industry Standards Board, formed in 1994, with the consolidation completed in 2002 as NAESB took on the broader cross-fuel and electric standards mandate. Each NAESB nomination cycle has a deadline by which shippers must submit their nomination for the gas day and a confirmation window during which the pipeline confirms or modifies the nomination based on capacity availability.

The five cycles, all in Central Time and applicable to the gas day that runs from 9:00 AM CT on the calendar day of flow to 9:00 AM CT the following day:

- Timely nomination. Deadline 1:00 PM CT the day before flow. Confirmation by 4:30 PM CT the same day. The Timely cycle is the largest by volume and accounts for the majority of regularly scheduled flow.

- Evening nomination. Deadline 6:00 PM CT the day before flow. Confirmation by 10:00 PM CT.

- Intraday 1 (ID1). Deadline 10:00 AM CT day of flow. Confirmation by 2:00 PM CT.

- Intraday 2 (ID2). Deadline 2:30 PM CT day of flow. Confirmation by 6:30 PM CT.

- Intraday 3 (ID3). Deadline 7:00 PM CT day of flow. Confirmation by 9:00 PM CT.

The five cycles serve different operational purposes. The Timely cycle is the day-ahead workhorse, the cycle in which an LDC’s procurement desk schedules baseload nominations against the next-day load forecast and a power generator nominates fuel for the next-day RTO market clearing. The Evening cycle absorbs late updates after the RTO day-ahead market clears in the afternoon and after the LDC’s revised weather forecast comes in. The three intraday cycles allow shippers to adjust nominations in response to weather forecast updates, real-time power dispatch, LNG cargo loading schedules, and operational disruptions. Each cycle runs a separate scheduling pass on the pipeline’s nomination engine, allocates available capacity to confirmed nominations under the firm-versus-interruptible priority order, and posts the confirmed flows to each shipper’s electronic bulletin board account.

The pipeline’s SCADA system measures actual flow at receipt and delivery meters in real time. Imbalances between confirmed nominations and actual flow are the difference between what the shipper said it would deliver or take and what physically moved through the meter. Small imbalances are normal; pipelines tolerate single-digit-percent imbalances on a daily basis without penalty. Persistent or large imbalances trigger tariff penalties scaled to the size of the imbalance and to the operational stress on the pipeline. Some pipelines reconcile imbalances at the end of each gas day; others accumulate them to a monthly imbalance account, with cash-out provisions at month-end based on a tariff-defined index price.

The NAESB cycle architecture is the operational rhythm of the US gas market. Every firm transport nomination, every capacity release confirmation, every storage injection or withdrawal schedule, and every LNG feedgas delivery passes through one of the five windows on the way from a paper contract to a metered molecule.

Operational Flow Orders and the Curtailment Hierarchy

When a pipeline cannot maintain operational integrity (line pack pressure, system balance, or delivery capacity at a given point), the operator issues an Operational Flow Order. OFOs are tariff-defined directives that require shippers to take corrective action within a specified window, with financial penalties for non-compliance. Three OFO categories cover most US interstate practice.

A Type 1 or Warning OFO is a notification that the pipeline is approaching an operational constraint. No financial penalty applies, but shippers are required to bring nominations into balance with their actual receipt and delivery activity. Warning OFOs are common in shoulder seasons when storage cycles, pipeline maintenance, or weather forecast revisions push line pack toward upper or lower operational limits.

A Critical Day OFO is a binding directive that requires shippers to deliver or take exactly their confirmed nomination, with no daily imbalance tolerance. Penalties for over-delivery and under-delivery typically run $5 to $25 per MMBtu in 2024 tariffs, scaled to the magnitude of the imbalance and to the duration of the OFO. Critical Day OFOs are common during polar vortex events, hurricane shut-ins on Gulf Coast pipelines, and infrastructure outages including compressor station failures and unplanned maintenance.

A Force Majeure declaration is the pipeline’s notice of an event beyond its operational control: a compressor station fire, a pipeline rupture, a severe weather event that shuts in upstream production, or a regulatory action that forces a service interruption. Force Majeure suspends contractual obligations on the affected segment for the duration of the declared event, protects the operator from breach-of-contract claims, and triggers re-routing of confirmed nominations onto alternative paths where capacity is available.

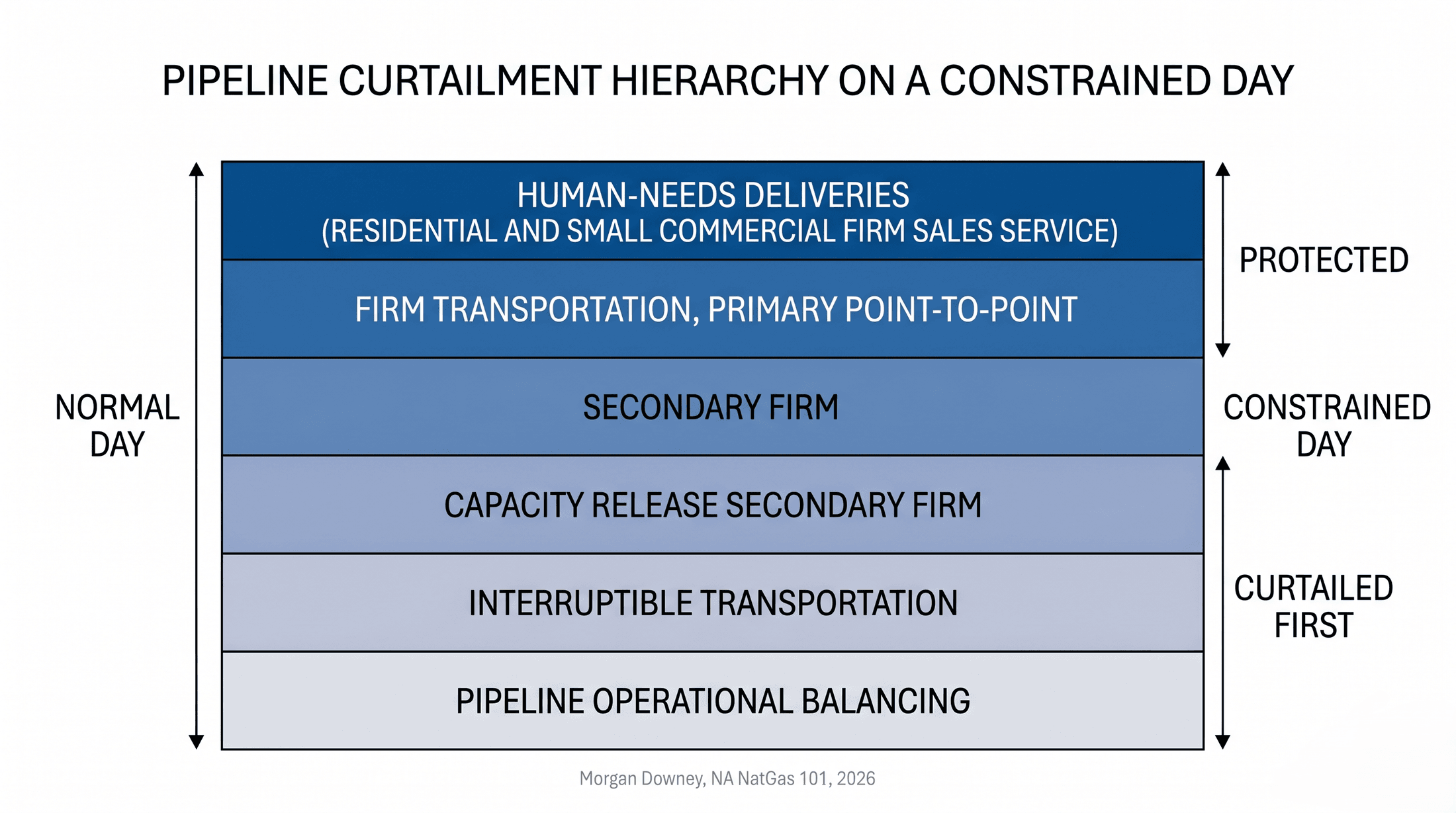

The curtailment hierarchy on a constrained day is encoded in pipeline tariffs and is consistent across most US interstate pipelines under the FERC tariff precedent that emerged from Order 636 and its post-1993 refinements:

- Highest priority: human-needs deliveries (residential and small-commercial firm sales-service customers that depend on the LDC for primary heat).

- Next: firm transportation customers with primary point-to-point rights.

- Next: secondary firm.

- Next: capacity release secondary firm.

- Next: interruptible transportation.

- Lowest: pipeline operational balancing (the pipeline can use its own gas to balance the system at the expense of all shipper classes).

The hierarchy was tested in three benchmark events. The January 2014 polar vortex forced multiple Northeast and Mid-Atlantic pipelines into Critical Day OFOs and curtailed substantial interruptible and capacity-release volume; the post-event PJM analysis identified gas-fired generator fuel-supply curtailment as a primary driver of the system’s 22 percent forced outage rate, alongside frozen instrumentation and mechanical trips. The January 2018 bomb cyclone produced similar curtailments on Algonquin Gas Transmission, Tennessee Gas Pipeline, and Texas Eastern. The February 2021 Winter Storm Uri shut in roughly 30 percent of Texas dry gas production at peak and forced ERCOT and the Texas intrastate pipeline grid into curtailments that cascaded through the power grid. The Uri curtailment hierarchy mattered because the gas-fired generators that dispatched were precisely those that had procured firm transport on intrastate pipelines, and the units that did not run included generators that had relied on interruptible service or on capacity-release positions junior to LDC recall.

The structural lesson from the three events is that the contract layer is the determinant of who runs and who does not on the most operationally stressed days of the year.

Negotiated Rates, Recourse Rates, and the Tariff Cap

Pipeline tariffs file two parallel rate structures. Recourse rates are the maximum rates approved in the pipeline’s most recent FERC rate case under cost-of-service rate-making. The recourse rate is available to any qualifying shipper as a default option and serves as the contractual fallback when a shipper does not negotiate a custom rate. Negotiated rates are agreed bilaterally between the pipeline and a specific shipper for a specific contract, with a rate that can be higher or lower than the recourse rate. New pipeline precedent agreements typically include negotiated rates structured around the project’s all-in economics, with the rate set to recover the project’s debt service, equity return, and operating costs over the contract tenor. Legacy contracts on long-established mainlines are often at recourse rates.

Negotiated rates are filed with FERC and made publicly available for the duration of the contract; the public filing prevents undisclosed price discrimination against similarly situated shippers. The disclosure requirement is the central enforcement mechanism for the non-discrimination principle that anchors the open-access framework. A shipper bidding into a capacity release auction can read the published negotiated rates on the pipeline at the same and adjacent points and price its bid accordingly.

The recourse rate is the pipeline’s tariff cap on capacity release transactions for releases longer than one year, after the Order 712 elimination of the cap on shorter releases. The recourse rate is also the reference rate for shipper substitution rights and for the regulated cost-of-service tariff applied to non-precedent-agreement shippers. A pipeline whose recourse rate sits substantially above market clearing will see most of its capacity move under negotiated rates, with the recourse rate functioning as a ceiling that few transactions touch. A pipeline whose recourse rate sits below market clearing will see firm shippers retain their capacity and use the capacity release market to capture the upside; the recourse rate becomes an effective price ceiling on long-term transactions, and the short-term release market clears higher under the Order 712 framework.

The tariff cap structure is one of the central regulatory mechanisms preventing pipelines from exercising market power on captive shippers. It limits the rate signal that would otherwise encourage new pipeline construction in tight markets, the structural tension that anchors the post-2014 Northeast pipeline scarcity covered in Chapter 10. The recourse rate is not the market-clearing price. It is the regulated ceiling against which the market clears.

The Order 636 Compliance Deadline, November 1993

On Mon Nov 1, 1993, the major US interstate gas pipelines completed the FERC-mandated transition to open-access transportation under Order 636. Each pipeline filed a restructured tariff separating merchant gas sales from transport service, offered firm transportation on a non-discriminatory basis to any qualifying shipper at the same receipt and delivery points, allocated its existing book of bundled merchant contracts among the new transport tiers, and exited the merchant business entirely.

The transition was contentious. Producers sued. LDCs sued. State regulators sued. The DC Circuit Court of Appeals upheld Order 636 in July 1996 in United Distribution Companies v. FERC, with modifications to the cost-recovery treatment of the pipelines’ stranded merchant-portfolio costs. Most pipelines absorbed several billion dollars of stranded costs against their rate base, with recovery allocated across LDCs and end-users through a transition cost surcharge that ran off over an extended horizon.

Before November 1993 the pipeline owned the molecule. After November 1993 the LDC owned the molecule, the pipeline owned the pipe, and a new market in transport contracts and capacity release filled the space between. The architecture of every section in this chapter dates to that month.

The contract layer determines who moves the molecule. Chapter 17 turns to the regulatory architecture that built that layer, and to the federal and state environmental and methane policy framework that now shapes what the layer is allowed to deliver.