Regulation and Environment

FERC, state utility commissions, methane emissions standards, EPA OOOOb/c, the EU import standard, and the regulatory architecture that prices methane intensity.

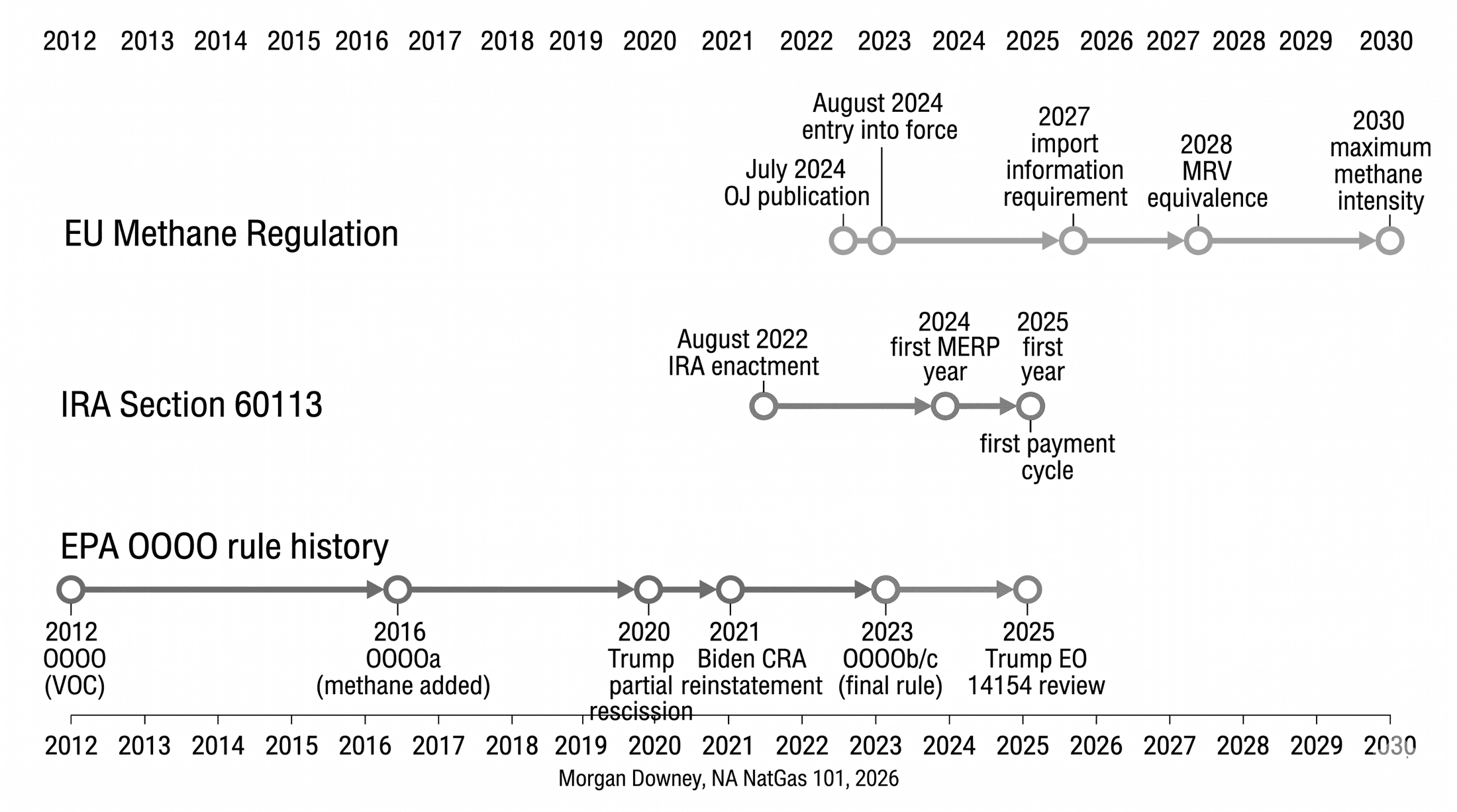

The Official Journal of the European Union published Regulation 2024/1787 on methane emissions reduction in the energy sector on Mon Jul 15, 2024. The text ran to 75 articles across roughly 80 pages of legal language. Twenty days later, on Sun Aug 4, 2024, the regulation entered into force across the 27 member states. The European domestic provisions began their phased implementation on the same day. The provisions that reach outside the EU’s borders, the part that touches US wellheads, would not bind for another three years.

The phased schedule is the part that moves the US Gulf Coast. Beginning in 2027, importers of natural gas, oil, and coal into the EU will be required to report on the methane emissions associated with the imported fuel and to confirm the originating producer applies a measurement, reporting, and verification framework to its emissions data. Beginning in 2028, the importer must demonstrate that the upstream MRV framework applied to the imported fuel is equivalent to the EU domestic standard. Beginning in 2030, imports that exceed a maximum methane intensity value, set by the European Commission through delegated acts, will face restrictions.

Cheniere Energy operates the Sabine Pass and Corpus Christi liquefaction terminals. Venture Global LNG operates Calcasieu Pass and Plaquemines. Sempra Infrastructure operates Cameron LNG. ExxonMobil and QatarEnergy operate Golden Pass. Each of these operators has long-term sale and purchase agreements with European utility buyers, and each of those agreements is now exposed to a piece of European law that did not exist before Sun Aug 4, 2024. The methane intensity of a US gas molecule, measured at the wellhead in the Marcellus or the Permian, transferred through gathering and processing, moved through the interstate pipeline system, liquefied at the export terminal, loaded onto a carrier, and discharged at a regasification terminal in the Netherlands or Spain, is now a regulated parameter in a foreign jurisdiction.

The chapter that follows is the regulatory architecture that the molecule passes through. Federal, state, international. Old, new, and being rewritten in real time.

The Federal Regulatory Stack

The federal architecture for natural gas is fragmented across five agencies. Each operates under its own statutory mandate. None of them was designed to act as a unified gas-industry regulator. The fragmentation is structural, not accidental.

The Federal Energy Regulatory Commission, FERC, regulates interstate gas transportation, interstate sales for resale, and LNG export terminal siting under the Natural Gas Act of 1938 and its subsequent amendments. The Section 7 certificate covered in Chapter 10 is the regulatory predicate for any new interstate pipeline or major expansion project. The Section 4 and Section 5 rate case framework also covered in Chapter 10 governs how pipeline tariffs are set and changed. Order 636 unbundling, addressed in Chapter 10, and Order 712 capacity release reform, addressed in Chapter 16, are the two structural reforms that built the modern interstate pipeline market. FERC’s jurisdiction stops at the LNG terminal fence on the export side and at the LDC city gate on the distribution side. Beyond those two points, state regulation takes over.

The Department of Energy’s Office of Fossil Energy and Carbon Management authorizes LNG exports to Free Trade Agreement and non-Free Trade Agreement countries under Section 3 of the Natural Gas Act. The non-FTA pause that the Biden administration imposed on Fri Jan 26, 2024 and that the Trump administration lifted on Mon Jan 20, 2025 is the most consequential DOE export-authorization decision in the history of US LNG. Chapter 14 covered both the pause and the unpause in detail. The DOE’s authorization is the federal permit that determines whether a US LNG molecule can clear customs at the export terminal. FERC permits the terminal; DOE permits the cargo.

The Pipeline and Hazardous Materials Safety Administration, PHMSA, sits within the Department of Transportation. PHMSA regulates interstate and intrastate gas pipeline safety under 49 CFR Part 192 and underground gas storage facility integrity under 49 CFR Part 193. The Aliso Canyon leak in 2015 and 2016, which Chapter 11 covered as the pivot point for the modern storage safety regime, drove PHMSA’s December 2016 underground gas storage rule. PHMSA’s other principal jurisdictional product is the integrity-management program required for transmission pipelines, with the periodic inspection cycle scaled to pipeline class and operating pressure. PHMSA enforcement is principally administrative; the agency issues civil penalties, corrective action orders, and consent decrees and refers criminal matters to the Department of Justice.

The Environmental Protection Agency regulates air emissions from oil and gas facilities through multiple overlapping authorities. The Clean Air Act New Source Performance Standards, codified at 40 CFR Part 60 Subpart OOOO and its successors, are the principal federal vehicle for methane regulation and the central topic of this chapter. The EPA Greenhouse Gas Reporting Program at 40 CFR Part 98, including the oil and gas Subpart W reporting rule, is the data backbone for federal methane policy and for the IRA Waste Emissions Charge. The Clean Air Act Section 111 authority that underpins the NSPS rule was the subject of the 2022 Supreme Court decision in West Virginia v. EPA, which narrowed the application of the Major Questions Doctrine to EPA rulemaking and constrained the agency’s ability to issue economy-wide emissions caps under Section 111(d) without explicit Congressional direction. EPA’s other gas-relevant rules cover hazardous air pollutants under the National Emission Standards for Hazardous Air Pollutants framework and ozone non-attainment designations under the State Implementation Plan process.

The Bureau of Land Management within the Department of the Interior regulates federal-land oil and gas leasing, royalty rates, and the conditions of operation on the roughly 245 million acres of federal surface and 700 million acres of subsurface mineral estate that the federal government manages. The BLM Methane Waste Prevention Rule, originally finalized in November 2016, partially rescinded in 2018, vacated by the Tenth Circuit in 2020, and re-issued in updated form in 2024, governs methane venting and flaring on federal acreage. BLM jurisdiction is consequential in New Mexico, Wyoming, Colorado, Utah, and the Mountain West states where federal acreage drives a substantial share of oil and gas production.

Coordination across the five agencies happens through informal inter-agency processes and through Congressional oversight rather than through any unified gas-industry regulator. The Trump administration in the 2017-2021 term and again in the 2025-onward term has used the executive order as the principal coordinating instrument; the Biden administration in 2021-2025 used inter-agency working groups and the Office of Information and Regulatory Affairs at OMB as the coordinating venues. None of these mechanisms has the statutory authority of a unified regulator. The fragmentation across the five agencies is the operating structure within which the methane policy stack has been built.

State Public Utility Commissions and the LDC Layer

Below the federal layer sit the state public utility commissions that regulate intrastate gas distribution. Each of the 50 state PUCs regulates the LDC service territories within its jurisdiction. The PUC sets the LDC’s allowed return on equity, approves the rate base, sets the cost-of-service tariffs by customer class, and reviews capital programs. Chapter 13 covered the LDC rate-case framework, the design-day standard for resource adequacy planning, and the cost-of-service mechanics in detail.

State PUC jurisdiction extends to several adjacent commercial and operational decisions. The PUC reviews and approves LDC procurement strategies, including the long-term firm transportation contracts the LDC signs with interstate pipelines under the framework covered in Chapter 16. The PUC sets the interruptible-versus-firm tariff hierarchy for end-user classes, with residential and small-commercial customers typically taking firm service at the highest priority and large industrial customers taking some mix of firm and interruptible. The PUC reviews purchased gas adjustment mechanisms, the regulatory device that passes through the LDC’s commodity cost of gas to retail customers without the lag of a full rate case. Some PUCs run formal commodity cost reviews quarterly; others run them annually.

The fragmentation across 50 state regulators produces 50 different versions of the LDC commercial model. The California Public Utilities Commission, the New York Public Service Commission, the Massachusetts Department of Public Utilities, and the Washington Utilities and Transportation Commission have taken the lead on building electrification proceedings, the regulatory venue in which the long-term role of natural gas in the residential and small-commercial heating sector is being adjudicated. Chapter 13 covered the New York All-Electric Buildings Act of May 2023 and the Berkeley Ninth Circuit decision that overturned the city’s 2019 gas-ban ordinance under federal preemption grounds. The state PUCs in Texas, Louisiana, Oklahoma, and the Mountain West states have taken the lead on reliability proceedings, the regulatory venue in which the resource adequacy and weatherization implications of Winter Storm Uri in February 2021 have been adjudicated. Chapter 12 covered the Public Utility Commission of Texas’s reliability orders and the Texas Railroad Commission’s gas weatherization rules.

The state PUC layer is the regulator the residential gas customer actually deals with. The federal layer governs the molecule’s interstate journey; the state layer governs the bill on the kitchen table.

EPA Subpart OOOO and the Methane NSPS Framework

The EPA’s New Source Performance Standards for the oil and gas sector are codified at 40 CFR Part 60 Subpart OOOO and its alphabet-suffix successors. The original Subpart OOOO, finalized on Tue Apr 17, 2012 and effective in October 2012, was the first federal NSPS to cover the oil and gas sector at the production, gathering, processing, transmission, and storage stages. Subpart OOOO regulated volatile organic compound emissions from new and modified sources, with the principal control technologies being zero-bleed pneumatic controllers, vapor recovery on storage tanks, and reduced emission completions on hydraulically fractured wells. Methane was not directly regulated under the original Subpart OOOO; the rule’s methane reductions were a co-benefit of the VOC controls.

Subpart OOOOa, finalized on Thu May 12, 2016 in the Obama administration’s “EPA New Source Performance Standards 2016,” directly added methane as a regulated pollutant for new and modified sources constructed or modified after Fri Sep 18, 2015. The control technology requirements expanded to cover quarterly leak detection and repair (LDAR) at gathering and boosting compressor stations, semiannual LDAR at well sites, and an emissions-based limit on hydraulic fracturing flowback. Subpart OOOOa was the first federal rule to directly regulate methane emissions from the oil and gas sector under Clean Air Act Section 111(b) authority.

The Trump administration partially rescinded Subpart OOOOa in two stages in 2020. The August 2020 “policy rule” removed the transmission and storage segment from the regulated source category and rescinded methane regulation entirely while retaining VOC controls. The September 2020 “technical rule” loosened LDAR frequency requirements at well sites and gathering compressor stations. The Biden administration restored methane regulation through a Congressional Review Act resolution signed by President Biden on Wed Jun 30, 2021, which disapproved the Trump 2020 rules and reinstated the 2016 Subpart OOOOa requirements.

The principal federal methane rule in force at the start of 2026 is the EPA’s December 2023 final rule package, which included Subpart OOOOb for new sources and Subpart OOOOc for existing sources. EPA Administrator Michael Regan signed the final rule on Sat Dec 2, 2023; the rule was published in the Federal Register on Mon Mar 8, 2024. Subpart OOOOb applies to sources constructed, reconstructed, or modified after Tue Dec 6, 2022; Subpart OOOOc applies to existing sources constructed before that date.

The OOOOb new-source standards include a phased-in zero-emission well completion standard, mandatory LDAR at fugitive-emission frequencies of bimonthly to quarterly depending on facility size and complexity, a routine flaring prohibition for associated gas at oil wells with limits on the volumes that may be flared rather than captured, zero-emission pneumatic controller requirements, dry-seal requirements for new centrifugal compressors, and a Super-Emitter Response Program that authorizes EPA-certified third parties to identify large emission events from satellite or aerial surveys and to require operators to investigate and repair within specified timeframes. The Super-Emitter Response Program is the first federal rule to formally incorporate satellite-derived emissions data into a binding regulatory action.

Subpart OOOOc requires states to develop implementation plans within two years of EPA’s rulemaking, with the state plans then subject to EPA approval. The state-plan timeline is a significant compliance lever; states like Colorado and New Mexico, which already operate methane rules at or above the federal floor, expected fast-track approval. States with no existing methane rule, including Texas, Louisiana, Oklahoma, and West Virginia, faced a more substantive plan-development burden.

The EPA estimated that the OOOOb/c rule package would prevent roughly 58 million metric tons of cumulative methane emissions through 2038, equivalent on a 100-year global warming potential basis to approximately 1.5 billion metric tons of CO2-equivalent over the rule’s life. Industry compliance cost estimates ran to roughly $14 to $19 billion over the rule’s first ten years. The OOOOb/c package was the most consequential federal methane rule ever issued for the oil and gas sector. The Trump 2025 administration directed EPA to review the rules through Executive Order 14154 on Mon Jan 20, 2025; the formal rescission would require notice-and-comment rulemaking and is likely to face legal challenge in either direction.

The IRA Methane Fee: The Waste Emissions Charge

The Inflation Reduction Act of 2022, signed by President Biden on Tue Aug 16, 2022, included a Methane Emissions Reduction Program at Section 60113. The MERP is structured as a hybrid: a Waste Emissions Charge that imposes a per-ton fee on excess methane emissions and a $1.55 billion grant program that funds emissions-reduction projects, methane monitoring infrastructure, and orphan-well plugging. The charge and the grant program operate as a fee-and-rebate structure: producers that exceed the facility-level waste emissions threshold pay the charge, while the grant program funds the technology and infrastructure that allow producers to reduce emissions below the threshold.

The Waste Emissions Charge applies to facilities reporting more than 25,000 metric tons of carbon dioxide equivalent annual emissions to the EPA Greenhouse Gas Reporting Program under Subpart W (the oil and gas sector reporting rule). The charge is calculated against a facility-level waste emissions threshold defined by facility type. The thresholds are expressed as a methane intensity ratio: total methane emissions divided by the volume of natural gas sent to sale or, in some categories, divided by the total volume of oil and gas produced. Facilities with intensity below the threshold pay nothing. Facilities with intensity above the threshold pay the charge on the excess methane volume only.

The charge schedule is statutory. The rate began at $900 per metric ton of methane for emissions in calendar year 2024, payable in 2025. The rate stepped up to $1,200 for 2025 emissions and to $1,500 for 2026 and subsequent years. The schedule is not indexed to inflation. The Trump 2025 administration directed EPA to review the MERP implementing rule through Executive Order 14154, but the statutory charge itself is embedded in the IRA and would require Congressional action to repeal.

The first payment cycle in the spring of 2025 produced a documented industry response. Producer 10-K disclosures filed in February and March 2025 reported first-cycle MERP liabilities ranging from a few million dollars at low-intensity producers to several tens of millions at higher-intensity operators. The Permian Basin operators with extensive associated-gas flaring at the wellhead reported the largest per-barrel charges; the Marcellus and Haynesville producers with gas-only operations and modern equipment reported smaller charges or, in some cases, no liability at all.

The structural effect of the MERP is to price methane intensity. A producer running modern zero-bleed pneumatic devices, vapor recovery, electric compression, and tight LDAR cycles incurs a small or zero charge. A producer running older equipment with leaky pneumatics, extensive routine flaring of associated gas, and infrequent leak inspections incurs a per-ton tax on the excess methane emitted at every facility above the threshold. The MERP did not estimate methane intensity. It priced it.

State Methane Regulation and Voluntary Certification

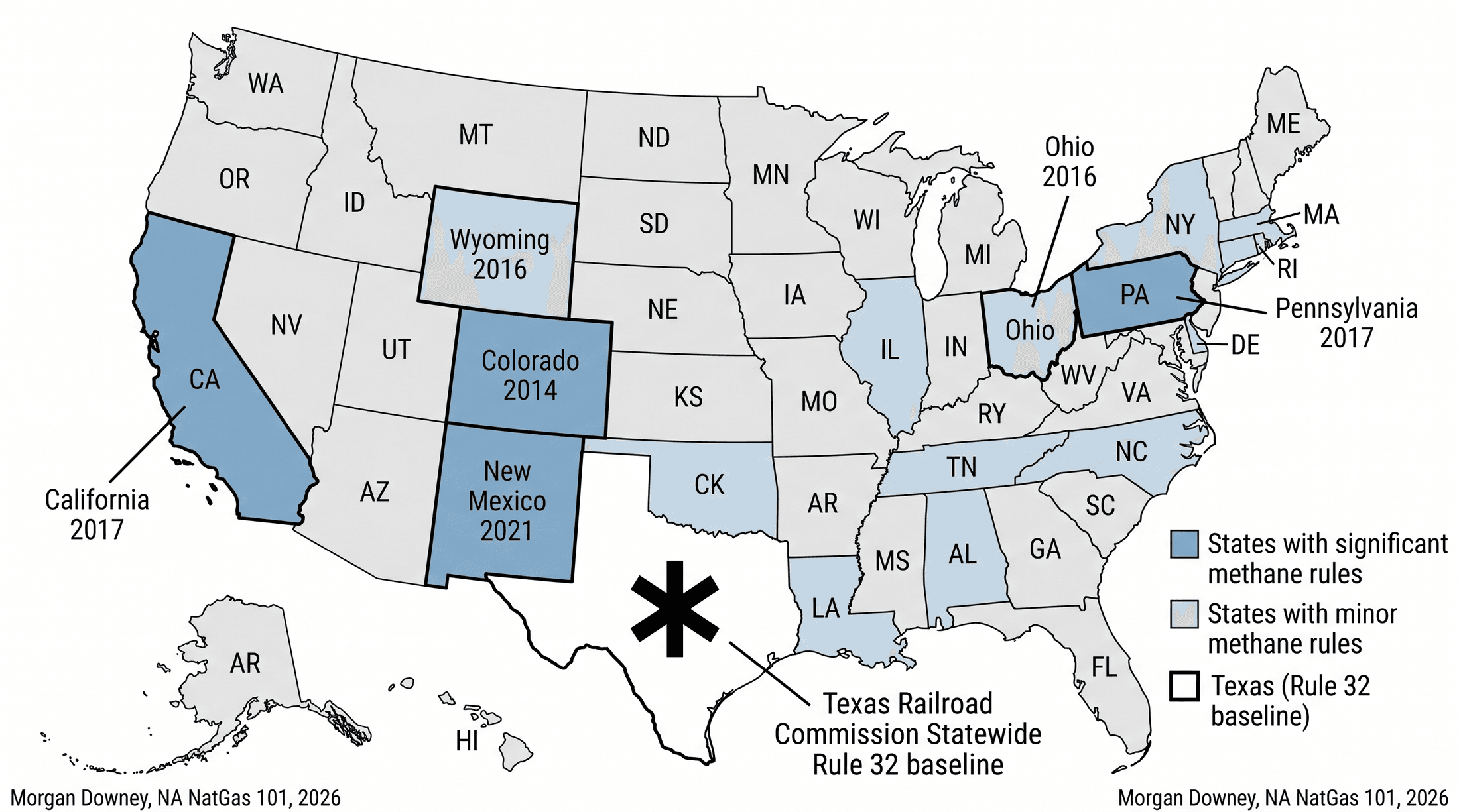

Several US states have built methane regulatory programs that go beyond the federal NSPS framework. The Colorado Air Quality Control Commission has issued leak-detection-and-repair, flaring, and pneumatic-device rules since February 2014, when the AQCC adopted the Regulation 7 update that imposed monthly to quarterly LDAR requirements at oil and gas facilities and zero-bleed pneumatic device requirements at new installations. Colorado’s 2014 rule was the first state methane rule in the US oil and gas sector and was widely cited as the technical template for the EPA’s 2016 Subpart OOOOa. The Colorado AQCC expanded the rule in 2017 to cover existing sources, in 2019 to require statewide methane intensity reductions through Senate Bill 19-181 and the subsequent rulemakings, and in 2021 to require pre-production leak detection at new well pads.

New Mexico’s Energy, Minerals and Natural Resources Department adopted methane rules in 2021 covering venting limits, flaring restrictions, and leak detection at new and existing wells in the Permian and San Juan basins. The New Mexico Environment Department’s separate ozone non-attainment rules, finalized in 2022, overlay the EMNRD venting rules to produce the most stringent state methane regime outside Colorado.

The Texas Railroad Commission, the principal regulator of oil and gas operations in Texas, has historically operated a less restrictive regulatory regime, with rule-based caps on flaring of associated gas under Statewide Rule 32 and limited LDAR requirements. Texas accounts for roughly 40 percent of US crude production and roughly 25 percent of US gas production. The state-level regulatory baseline in the Permian portion of Texas is therefore the binding constraint on a substantial share of total US oil and gas methane emissions.

The California Air Resources Board has operated a comprehensive oil and gas methane rule since March 2017, with quarterly LDAR, pneumatic device requirements, and a separate Greenhouse Gas Mandatory Reporting Regulation that overlays the federal Subpart W reporting.

State-level methane rules are typically the layer at which the binding constraint sits in advance of federal rule-making, with states leading and federal rules following. The Trump 2025 federal rollback does not affect the state programs; the Colorado, New Mexico, and California rules continue to operate independently of federal action.

Voluntary certification programs run alongside the regulatory layer. The MiQ standard, developed jointly by the Rocky Mountain Institute (RMI) and SYSTEMIQ and published in early 2020, issues independent third-party methane intensity certifications on a Grade A through D scale, with Grade A representing facility-level methane intensity below 0.05 percent and Grade D representing intensity above 1.0 percent. Producers with Grade A or B certification can market their gas as “responsibly sourced gas” (RSG) at a small premium to uncertified gas. The MiQ-certified US producer roster as of 2024 and 2025 included EQT (the largest US gas producer by volume), Coterra Energy, Range Resources, Antero Resources, Chesapeake Energy, and a substantial portion of Equinor’s US production. Other competing certification frameworks include Project Canary’s TrustWell standard and the GTI Energy Veritas protocol. Colorado wrote the rule. EPA followed. The market now writes the certificate.

The EU Methane Regulation and the Import Standard

The European Union published Regulation 2024/1787 on methane emissions reduction in the energy sector in the Official Journal of the European Union on Mon Jul 15, 2024, with entry into force on Sun Aug 4, 2024. The regulation is the first comprehensive EU-level methane emissions regulation for the energy sector; previous EU emissions regulation operated through the Emissions Trading System for installations and through national-level reporting under the Effort Sharing Regulation for diffuse sources.

The regulation imposes measurement, reporting, and verification (MRV) requirements on EU domestic oil, gas, and coal operations. The MRV requirements include facility-level measurement of methane emissions on a regular cycle, third-party verification of the measurement data, mandatory leak detection and repair at all facilities, a phased ban on routine venting and flaring with limited operational and safety exceptions, and a requirement to identify and address inactive, temporarily plugged, and permanently plugged and abandoned wells. The domestic provisions began phased implementation in 2024 and 2025 and are scheduled to reach full effect in 2027.

The provisions that reach outside the EU’s borders are the import provisions. Beginning Sat Jan 1, 2027, importers of natural gas, oil, and coal into the EU will be required to report on the methane emissions associated with the imported fuel, including upstream methane intensity at the production site, and to confirm that the originating producer applies an MRV framework to its emissions data. Beginning in 2028, the importer must demonstrate that the upstream MRV framework applied to the imported fuel is equivalent to the EU domestic standard. Beginning in 2030, imports that exceed a maximum methane intensity value, set by the European Commission through delegated acts, will be subject to financial penalties or other restrictions.

The maximum methane intensity values for imports will be set by the Commission through delegated acts adopted between 2027 and 2029, with the level expected to track EU domestic production intensity. The expected threshold range is in the area of 0.2 percent methane intensity at the wellhead for natural gas, give or take, but the specific values have not been finalized as of early 2026.

The regulation reaches US LNG exporters through the buyer relationship. Cheniere Energy, Venture Global LNG, Sempra Infrastructure, ExxonMobil and QatarEnergy at Golden Pass, Freeport LNG, and the smaller US Gulf Coast operators sell LNG to European utilities including Naturgy, ENGIE, Shell European Trading, BP Gas Marketing, EDF, Uniper, RWE, Eni, and others. The US-to-Europe LNG trade has averaged roughly 7 to 9 billion cubic feet per day in 2024 and 2025, depending on month, with Europe absorbing the majority of US LNG cargoes after the 2022 cutoff of Russian pipeline gas. The European utility buyer is now contractually obligated to verify that the methane intensity of the cargo it purchases will be below the EU threshold by 2030, and that requirement has propagated upstream through long-term sale and purchase agreements signed since the regulation entered into force.

Compliance documentation, third-party certification (MiQ, Project Canary, GTI Veritas, or operator-specific equivalents), and chain-of-custody tracking from wellhead to ship are the practical mechanisms. The regulation has been criticized by US industry groups, including the American Petroleum Institute and the Center for LNG, as an extraterritorial application of EU climate policy. It has been defended by environmental groups, including the Environmental Defense Fund and the Clean Air Task Force, as a necessary lever to reduce upstream methane emissions globally. Whatever the politics, the buyer-side requirement is now contractually embedded in long-term SPAs between US suppliers and European utility buyers, and the methane intensity of US Gulf Coast LNG cargo is now a tradeable parameter in the European spot market.

Spring 2025: The First MERP Payment Cycle

EQT Corporation, the largest US natural gas producer by volume, filed its 2024 annual report on Form 10-K with the Securities and Exchange Commission in February 2025. The financial statements disclosed a Waste Emissions Charge accrual under IRA Section 60113. EQT’s facility-level methane intensity, certified at MiQ Grade A across most of its Marcellus production, sat below the federal threshold at every reportable facility. The Waste Emissions Charge accrual was negligible. EQT did report compliance program costs, third-party verification fees, and additional LDAR cycles required to maintain certification, captured in the operating expense line.

Coterra Energy, with operations in both the Marcellus and the Permian, filed a similar disclosure several days later. Coterra’s Marcellus methane intensity sat below threshold; its Permian associated-gas operations sat above threshold at several facilities. The 2024 MERP charge accrual was reported in the low-tens-of-millions range.

The two filings, read side by side, were the first concrete documentation of the MERP’s structural effect. The price of methane intensity at the wellhead was no longer a forecast or a model output. It was a line item in the financial statements of the largest US gas producers, paid in cash to the United States Treasury, on a schedule that runs through 2026 and beyond.

The 2025 Political Inflection and the Durable Constraints

The Trump 2025 administration has signaled intent to dismantle the federal methane policy stack. Executive Order 14154, “Unleashing American Energy,” was signed by President Trump on Mon Jan 20, 2025, the first day of his second term. The order directed agency review of EPA’s OOOOb and OOOOc rules, the IRA MERP implementing rule, the BLM Methane Waste Prevention Rule, and the related federal methane reporting framework. Trump on the same day issued a second executive order, “Putting America First in International Environmental Agreements,” directing the second US withdrawal from the Paris Agreement under the United Nations Framework Convention on Climate Change. The first US withdrawal during the 2017-2021 Trump term took effect Wed Nov 4, 2020, the day after the November 2020 election; the Biden administration rejoined the agreement on Fri Feb 19, 2021. The second withdrawal will take effect one year after the formal notification.

The withdrawal of regulatory pressure at the federal level creates real space for producers operating on federal land or in states with permissive regulation. The OOOOb rule, the OOOOc state-plan deadlines, the MERP implementing details, and the BLM venting and flaring rule are all under EPA and DOI review. Notice-and-comment rulemaking would be required to formally rescind any of them, with the timetable likely running through 2026 and into 2027. Litigation in either direction is likely. The Biden-era rules have been challenged by industry groups since their 2023 issuance; the Trump-era rescissions, when they emerge, will be challenged by states (California, Colorado, New York, New Mexico) and by environmental groups under the Administrative Procedure Act and the Clean Air Act endangerment finding.

The constraint stack is not federal alone. The IRA Section 60113 charge is statutory and survives administrative action absent Congressional repeal. The current Republican-controlled Congress had not, as of early 2026, voted to repeal Section 60113, in part because the underlying IRA grant program is funding methane-monitoring and orphan-well infrastructure projects in Republican-leaning states including Texas, Wyoming, and Pennsylvania. The EU Methane Regulation is foreign law that reaches US LNG cargoes through the buyer relationship and cannot be affected by US executive or legislative action. The state-level methane programs in Colorado, New Mexico, and California operate independently of federal action and have been strengthened, not weakened, in 2025. The voluntary certification programs operate on producer-side commercial logic and on European buyer demand that survives any specific US administration. The European utility buyer’s contractual requirement for low-methane-intensity supply is a function of European buyer politics, ESG investor pressure, and EU regulatory deadlines that the US federal government cannot directly affect.

The structural argument is that methane emissions regulation has been built into a multi-layered architecture. Federal rules at EPA, BLM, and DOE. State rules at the AQCCs and PUCs in California, Colorado, New Mexico, and the building electrification states. International law at the EU. Voluntary certification at MiQ, Project Canary, and GTI Veritas. Buyer-side contractual requirements in long-term SPAs. Federal rules can be rescinded by executive order. State rules, foreign law, and buyer contracts cannot.

Chapter 1 opened with a Texas freeze that turned a regional weather event into a financial crisis because the gas system had no spare capacity, no second pipeline, and no substitute fuel that could show up by lunchtime. The fifteen chapters between then and now have unpacked why: the geology that puts the molecule under particular rocks, the chemistry that distinguishes methane from a barrel of oil, the captive infrastructure that delivers it, the demand seasonality that prices it, the end-use lock-in that holds the demand in place, and the methane intensity that now sits as a regulated parameter on cargoes loaded in Louisiana and discharged in Spain. This book has not covered OPEC+ politics at the source, the hydrogen and carbon-capture pathways that may sit on top of the gas value chain in the 2030s and 2040s, the global LNG supply curve outside North America, or the deeper policy debate around natural gas’s role in a 2050 net-zero economy; each merits its own treatment. The structural architecture holds whether or not any specific administration’s executive orders survive judicial review, and the molecule still has to move through the pipe.