The Players

Producers, oilfield services, gas processors, pipeline operators and the MLP era, storage operators, LNG operators, marketers and schedulers, banks, hedge funds and specialist traders, trading houses, exchanges and price reporting agencies, regulators, and industry associations.

On the morning of Wed January 22, 2014, an Arctic high-pressure system displaced the normal jet-stream pattern across North America and pushed temperatures along the Atlantic seaboard to levels not recorded in two decades. Boston Logan bottomed at minus 9 degrees Fahrenheit. Hartford reached minus 14. The gas-fired generation fleet across New England ran flat-out and the residential heating load hit the systemic peak of the year. The Henry Hub next-day spot settled that morning at $4.55 per million British thermal units. On the same day, the cash gas spot at the Algonquin Citygate, the New England delivered price published by S&P Global Platts and ICE, settled at roughly $77 per MMBtu, the highest single-day print in the history of the index up to that point. Two weeks later, on Wed February 5, the index printed above $120.

The basis differential of $73 was not a producer profit. The producer at the wellhead in Pennsylvania or Louisiana was selling gas at an index price set days earlier. The local distribution company at the Boston city gate was selling under tariff to its residential customers at regulated rates that bore no relationship to the cash market. The $73 was captured by intermediaries: gas marketers holding firm transportation capacity on the Algonquin and Tennessee Gas pipelines, schedulers releasing that capacity to second-tier marketers under FERC capacity-release rules, basis traders at hedge funds and bank derivatives desks long Algonquin basis swaps for two months going into the storm, and a handful of New England power plants that switched to oil for the day and resold their unused gas allocations into the cash market at the clearing price.

The molecule that delivered into a Boston residential meter that morning passed through a producer, a gathering operator, a processing plant, an interstate pipeline, a marketer, a scheduler, a clearinghouse, a price reporter, and a regulated distribution utility. Each one is a category. This chapter is the directory.

Producers and exploration-and-production firms

The upstream half of the gas business is dominated by a small number of public independents. EQT Corporation (NYSE: EQT) is the largest US natural gas producer, with production approximately 6.0 to 6.5 billion cubic feet equivalent per day. The company’s acreage is concentrated in the dry-gas window of the southwestern Marcellus and the wet-gas window of the Utica, in Pennsylvania, West Virginia, and Ohio. Its 2023 acquisition of Tug Hill and XcL Midstream and its 2024 acquisition of the remaining minority interest in Equitrans Midstream completed a vertical integration into gathering and processing that no other large gas producer has matched.

Antero Resources (NYSE: AR) is the second-largest dry-gas producer in Appalachia, with a heavy weighting toward the wet-gas Utica and a downstream NGL fractionation footprint connected to the Mariner East system. Range Resources (NYSE: RRC) drilled the first commercial Marcellus well, the Renz Number 1, in October 2004 and remains a top-five Appalachian producer. Coterra Energy (NYSE: CTRA), formed from the 2021 merger of Cabot Oil and Gas and Cimarex Energy, runs the largest concentrated dry-gas position in northeast Pennsylvania alongside a Permian oil business that funds the gas program through cycles. Expand Energy (NASDAQ: EXE), the post-merger entity from the 2024 combination of Chesapeake Energy and Southwestern Energy, is now the largest North American producer concentrated in the Haynesville and Marcellus gas basins by reserves. Comstock Resources (NYSE: CRK), majority-owned by Dallas Cowboys owner Jerry Jones, is a pure-play Haynesville operator. Gulfport Energy (NYSE: GPOR) operates in the Utica and SCOOP plays following its 2021 emergence from Chapter 11.

Among the integrated majors, ExxonMobil (NYSE: XOM) holds the largest single US gas position by virtue of its Permian associated-gas production and its 30 percent interest in Golden Pass LNG, the joint venture with QatarEnergy in Sabine, Texas. Chevron (NYSE: CVX) produces gas as a byproduct from the Permian and from a Haynesville position. Shell plc (NYSE: SHEL) inherited a substantial Appalachian position from its 2016 BG Group acquisition and divested most of it to National Fuel Gas Company (NYSE: NFG) in 2020. BP plc (NYSE: BP) operates the BPX Energy onshore subsidiary in the Permian, Eagle Ford, and Haynesville with a moderate gas weighting.

The privately held and private-equity-backed segment runs much of the rest. Ascent Resources, backed by Energy and Minerals Group and First Reserve, is one of the larger private Appalachian Utica producers. Aethon Energy is a Dallas-based Haynesville and Bossier producer that has held the largest private gas position in the play through several capital cycles. Encino Acquisition Partners, owned by the Canada Pension Plan Investment Board, runs the Utica position formerly held by Chesapeake. Hilcorp Energy is one of the largest privately held US oil and gas producers, with a large Cook Inlet, Alaska gas position, an Appalachian Marcellus position, and the producing properties acquired from BP Alaska in 2020.

Canadian gas-weighted independents are a separate cohort. Tourmaline Oil Corp. (TSX: TOU) is the largest Canadian natural gas producer, with production concentrated in the Alberta Deep Basin, the Montney, and the Peace River Arch. ARC Resources (TSX: ARX) operates a top-tier Montney position. Birchcliff Energy (TSX: BIR) runs a Montney-focused gas business. Ovintiv Inc. (NYSE: OVV; formerly Encana) is dual-listed in New York and Toronto with a balanced US Permian and Canadian Montney portfolio. Crew Energy and Tamarack Valley round out the mid-cap names.

The structural fact is concentration. Roughly 75 percent of US dry gas production now comes from twenty-five firms. The producer chapter of the gas business is a small chapter.

Oilfield service providers

The producer drills, completes, and pumps. The oilfield service contractor supplies the rig, the frac fleet, the directional steering tools, the proppant, and the field crews that do the actual physical work. Producer earnings calls now reference service-cost availability as the constraint on production growth above resource availability.

Three integrated firms dominate the international and integrated US service market. SLB (NYSE: SLB; formerly Schlumberger) is the largest oilfield-services firm globally and the technology leader in directional drilling, measurement-while-drilling, and reservoir characterization. Halliburton (NYSE: HAL) is the largest US-domestic services firm and the dominant pressure-pumping provider in the Lower 48. Baker Hughes (NASDAQ: BKR) operates a balanced portfolio across drilling services, completions, and production chemicals, plus a substantial industrial gas turbine business inherited from the 2017 GE Oil and Gas merger.

In US land drilling, Helmerich and Payne (NYSE: HP) is the largest contractor by AC-rig count and was the early scaler of the FlexRig design that became the industry-standard high-spec land rig. Patterson-UTI Energy (NASDAQ: PTEN), following its 2023 acquisitions of NexTier Oilfield Solutions and Ulterra Drilling Technologies, is the second-largest US land driller and a top-three pressure pumper. Nabors Industries (NYSE: NBR) operates a mixed US and international fleet. Precision Drilling Corporation (TSX: PD) is the dominant Canadian driller.

Pressure pumping, the term for the high-horsepower equipment fleet that pumps the slurry of water, sand, and chemicals downhole during a hydraulic fracture, is fragmented. Liberty Energy (NYSE: LBRT) and ProPetro Holding (NYSE: PUMP) are top-three publicly held pumpers. ProFrac Holding (NASDAQ: ACDC) is controlled by the Wilks family and runs an integrated frac, sand, and wireline business. Halliburton’s pressure-pumping fleet remains the largest single fleet by horsepower.

Sand and proppant are a separate vertical. US Silica Holdings was taken private by Apollo Global Management in July 2024. Smart Sand (NASDAQ: SND), Hi-Crush, and Covia Holdings round out the named operators. Most pressure pumpers source proppant from a mix of third-party silica suppliers and from in-basin sand mines that they operate themselves. The shift from Northern White sand transported by rail to in-basin Permian and Eagle Ford sand mined locally was a consequential cost reset around 2017 and 2018.

The schedule of rig releases and frac fleet deployments reported by Baker Hughes weekly and by Primary Vision biweekly is the leading indicator of US gas supply six to twelve months forward. Producers contract these crews on a multi-month basis; service firms publish utilization and pricing trends in their quarterly disclosures. The cycle of producer cash flow and service capital availability sets the marginal supply curve.

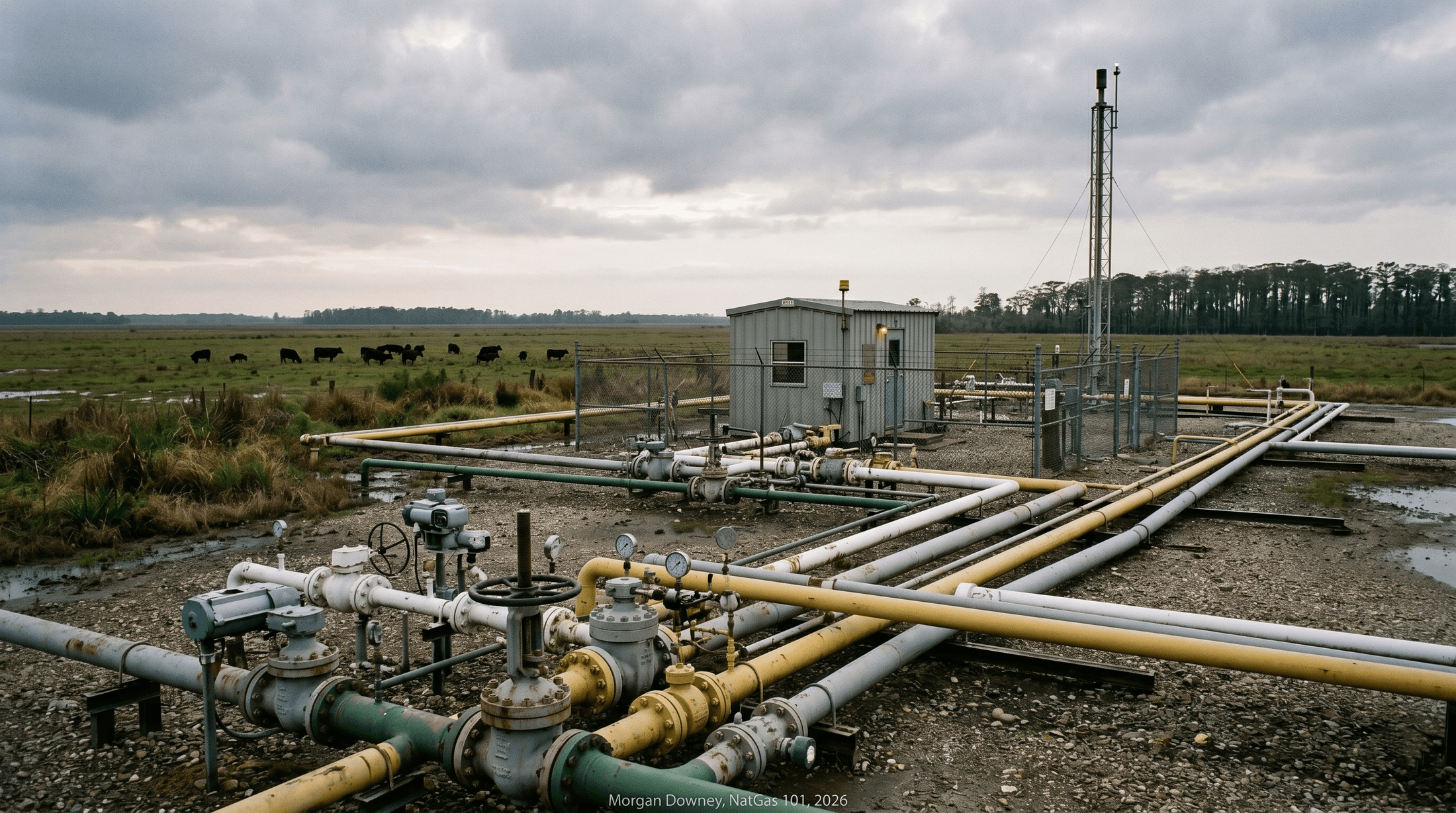

Gas gathering and processing

Once gas is produced from the wellhead, it must be moved to a treatment facility before it can enter an interstate pipeline. The molecule typically arrives at the wellhead with associated water vapor, carbon dioxide, hydrogen sulfide if the play is sour, and an entrained mix of natural gas liquids: ethane, propane, butane, isobutane, and pentanes-plus. The gathering operator owns the small-diameter wellhead pipe and the central treatment plants where the gas is dehydrated, sweetened if necessary, and stripped of NGLs to pipeline-quality specification.

Targa Resources (NYSE: TRGP) is one of the largest US gas processors by throughput, with the dominant Permian gathering and processing system, a major Eagle Ford position, and an NGL pipeline and fractionation business connecting Mont Belvieu to the Gulf Coast export docks. Enterprise Products Partners (NYSE: EPD) operates a vertically integrated gas processing, NGL pipeline, fractionation, and Gulf Coast LPG export business; it is the largest US midstream firm by EBITDA. MPLX (NYSE: MPLX), the master limited partnership operating Marathon Petroleum’s midstream assets, runs gathering and processing in the Marcellus, Utica, Permian, and Bakken. ONEOK (NYSE: OKE) acquired Magellan Midstream Partners in 2023 and completed its acquisition of EnLink Midstream in January 2025, building a continental footprint of NGL pipelines and processing plants from the Bakken through the Permian to the Gulf Coast.

The function of the gas processor is technical and capital-intensive. A modern cryogenic plant cools the gas stream to roughly minus 120 degrees Fahrenheit at elevated pressure, condensing the heavier hydrocarbons into a liquid stream while leaving methane in the gas phase. The methane is recompressed and delivered to the interstate pipeline. The NGL stream is routed by Y-grade pipeline to a Mont Belvieu fractionator. Custody of the molecule transfers from gathering to interstate pipeline at the processing plant tailgate. From that point the molecule has a published quality specification, a measured volume, and an interstate price.

Pipeline operators

Federal Energy Regulatory Commission Order 636, issued Wed April 8, 1992, made interstate pipelines common carriers. They no longer buy and resell gas. They sell transportation under tariff to anyone who holds firm capacity. The pipeline operators today are a small set of large public corporations.

Williams Companies (NYSE: WMB) operates the Transcontinental Gas Pipe Line, known as Transco, the largest US gas pipeline by throughput, running from south Texas through the Gulf Coast and up the eastern seaboard to New York City. Williams also operates the Northwest Pipeline serving the Pacific Northwest and the Sequent Energy gas marketing arm. Energy Transfer (NYSE: ET), through a series of acquisitions including Sunoco Logistics, USA Compression, Crestwood Equity Partners, and Enable Midstream, operates one of the largest integrated US natural gas, NGL, and crude oil pipeline networks. Kinder Morgan (NYSE: KMI) operates the largest US natural gas pipeline network by mileage at roughly 72,000 miles, including the Tennessee Gas Pipeline, the Colorado Interstate Gas system, the El Paso Natural Gas system, and the Natural Gas Pipeline of America.

Enbridge (NYSE: ENB), the Calgary-headquartered Canadian operator, completed its acquisition of three Dominion Energy gas distribution utilities (East Ohio Gas, Questar Gas, and Public Service Company of North Carolina) in 2024 and now operates one of the largest North American gas pipeline and distribution footprints. TC Energy Corporation (TSX: TRP), the Canadian-parented operator of the Columbia Gas Transmission and Columbia Gulf systems, completed the spin-off of its liquids pipelines business as South Bow Corporation (TSX: SOBO) on Tues October 1, 2024. Boardwalk Pipeline Partners, owned by Loews Corporation following the 2018 take-private transaction, operates the Texas Gas Transmission and Gulf South systems. DT Midstream (NYSE: DTM), spun off from DTE Energy in 2021, operates the NEXUS pipeline and Appalachian gathering assets.

The MLP era and its retreat. From 2014 through 2018, the master limited partnership structure was the dominant corporate form for US midstream firms, taking advantage of pass-through tax treatment and a yield-investor base that bid up partnership unit prices. The 2017 Tax Cuts and Jobs Act lowered the corporate tax rate to 21 percent, narrowing the differential that had driven the MLP advantage. Beginning in 2018, the major MLPs unwound their incentive distribution rights and consolidated back into C-corporations: Kinder Morgan rolled up its MLPs in 2014, ONEOK rolled up ONEOK Partners in 2017, Williams rolled up Williams Partners in 2018, and Enbridge rolled up Spectra Energy Partners and Enbridge Energy Partners in 2018 and 2019. The MLP structure persists today only in a handful of firms (Enterprise Products Partners, Energy Transfer, MPLX, Plains All American, Western Midstream).

Storage operators

Underground gas storage exists to balance the seasonal mismatch between roughly flat year-round production and heavily seasonal residential heating demand. Three categories of storage account for almost all working capacity: depleted oil and gas reservoirs, salt caverns, and aquifers.

Most depleted-reservoir storage is owned by the interstate pipeline that the storage system feeds. Williams operates a significant storage portfolio across the Transco system. Spectra Energy, now Enbridge, operates the Texas Eastern depleted fields. Tennessee Gas Pipeline (Kinder Morgan) operates a large storage book in the Appalachian basin. The local distribution company often owns the storage facility used to serve its peak-day load. National Fuel Gas, Consolidated Edison, and Southern Company Gas all own storage fields in their regional service territories.

Salt-cavern storage is mostly merchant. Boardwalk operates Petal Gas Storage and the Choctaw Hub in Mississippi. Bobcat Gas Storage at Port Barre, Louisiana is operated under Enbridge. Spire Storage West (subsidiary of Spire Inc., NYSE: SR) operates facilities in the Rockies. Enstor Energy, owned by ArcLight Capital, operates several merchant salt-cavern facilities in Texas and Mississippi. Sempra Infrastructure operates the Mississippi Hub and Bay Gas facilities.

The economic function of storage is the seasonal calendar spread. The summer-injection and winter-withdrawal cycle, hedged on the NYMEX strip, gives the operator a pre-locked margin. Storage operators sell firm and interruptible capacity to LDCs, marketers, and end users; the contract rate plus the calendar spread determines profitability. Total US underground storage working capacity of approximately 4.6 trillion cubic feet is the country’s single largest residential-heating buffer.

LNG operators

Eight US LNG export terminals are in commercial service as of early 2026 across five operators.

Cheniere Energy, Inc. (NYSE: LNG) operates Sabine Pass (Cameron Parish, Louisiana) and Corpus Christi (Texas), the two largest US LNG export terminals by liquefaction capacity. Sabine Pass started commercial exports on Wed February 24, 2016 and now operates six trains. Corpus Christi Trains 1 through 3 are in service; the Corpus Christi Stage 3 expansion (seven mid-scale trains) has been reaching substantial completion in stages through 2025 and 2026, with Train 1 substantially complete in March 2025 and the first five trains all complete by March 2026. Cheniere is the largest US LNG exporter by volume.

Venture Global, Inc. (NYSE: VG) operates Calcasieu Pass (Cameron Parish, Louisiana, in service 2022) and Plaquemines (Plaquemines Parish, Louisiana, in service 2024), and has Calcasieu Pass 2 under development. The firm completed an initial public offering in January 2025. The firm pioneered the modular mid-scale liquefaction train architecture and reached first cargo on materially shorter timelines than the prior generation of large-scale plants.

Sempra Infrastructure (subsidiary of Sempra, NYSE: SRE) operates Cameron LNG (Hackberry, Louisiana, in service 2019, three trains) and is constructing Port Arthur LNG (Texas) with Phase 1 in commissioning. Cameron is a partnership with Mitsui, Mitsubishi, Japan LNG Investment, and TotalEnergies. The ExxonMobil and QatarEnergy joint venture operates Golden Pass LNG (Sabine Pass, Texas), which loaded its first cargo in April 2026. Berkshire Hathaway Energy operates Cove Point LNG (Lusby, Maryland), the smaller export-and-storage facility on the Chesapeake Bay, acquired from Dominion Energy in 2020. Kinder Morgan operates Elba Island LNG (Chatham County, Georgia), a smaller-scale facility built around modular liquefaction units. Freeport LNG (Quintana Island, Texas) is privately held with significant Riverstone Holdings backing and operates three trains.

Two large projects are in development. NextDecade Corporation (NASDAQ: NEXT) is developing Rio Grande LNG at Brownsville, Texas, with Phase 1 (three trains) under construction by Bechtel following its July 2023 final investment decision; first LNG production is expected in 2027. Energy Transfer is developing Lake Charles LNG (Calcasieu Parish, Louisiana) with the FERC certificate received and final investment decision pending as of late 2025.

US LNG gross exports averaged approximately 11.9 billion cubic feet per day in 2024 and are running closer to 14 in 2025, with projections to reach roughly 24 to 26 billion cubic feet per day by 2028 as the Stage 3, Calcasieu Pass 2, Port Arthur, Golden Pass, and Rio Grande projects come online.

Gas marketers and schedulers

Order 636 unbundled the merchant function from the pipeline. The marketer is the firm that buys gas from producers, holds firm transportation capacity on interstate pipelines, schedules delivered volumes day by day, and sells delivered gas to LDCs and end users. The function is operationally intensive and credit-intensive, and it is where the daily price discovery of physical gas actually happens.

The largest North American gas marketers are mostly affiliated with majors and integrated utilities. BP Energy Company is the gas marketing arm of BP and consistently among the top US physical gas marketers by volume; Tenaska Marketing Ventures has held the top spot in the FERC Form 552 ranking for the past two years. Shell Energy North America is the gas-and-power marketing subsidiary of Shell, with a substantial Texas ERCOT power and natural gas book. EDF Trading North America is the US gas-and-power desk of Électricité de France. Tenaska Marketing Ventures is a privately held Omaha-based marketer with a long-standing producer-aggregation business and a large Texas industrial customer book. DTE Vantage (formerly DTE Energy Trading) is the marketing subsidiary of DTE Energy. Castleton Commodities International was originally spun out of the Louis Dreyfus Highbridge Energy desk in 2013. Macquarie Energy is the gas-and-power desk of Macquarie Group. Twin Eagle Resource Management is a privately held Houston-based marketer.

Voice and electronic brokers intermediate the trades that are not bilateral. TFS-ICAP, Tradition Financial Services, Marex, and several smaller specialty firms run the daily voice broker desks for cash gas, basis, and seasonal spreads. Most NYMEX and ICE cleared trades are voice-confirmed and electronically executed, with the broker holding both sides’ identities until the trade clears.

Capacity release is the unbundling instrument that ties the secondary capacity market to the daily molecule. The holder of firm transportation capacity who does not need it for the day or month posts the capacity for release on the pipeline’s electronic bulletin board. A second-tier marketer or end user with a delivery obligation buys the released capacity at a clearing rate, and the release reverts to the original holder at the end of the term. The aggregate capacity-release market clears tens of billions of dollars of transportation rights per year, and its bid-offer is the day-by-day expression of basis differentials across the US grid.

Banks and financial institutions

The bank physical-commodities business has retreated steadily since 2014. Macquarie Group (ASX: MQG) has filled most of the space that the Wall Street firms vacated. Macquarie Energy has eclipsed Goldman Sachs and Morgan Stanley to become one of the largest physical commodities desks on Wall Street by personnel and physical book size. The desk runs producer hedging, marketer financing, storage trading, and physical scheduling across natural gas, power, NGLs, and refined products.

Goldman Sachs’s J. Aron and Company commodities subsidiary, the storied physical desk that ran much of the US merchant power and gas trade through the 2000s, scaled back its physical activity in stages from the 2014 metal warehousing divestiture through 2019 metals retrenchment and now primarily runs a derivatives book. Morgan Stanley exited most of its physical commodities business after 2014 with the sale of its TransMontaigne refined-products subsidiary; it retained a derivatives book and a smaller physical natural gas franchise. JP Morgan Chase exited physical commodities in October 2014 with the sale of its global commodities physical business to Mercuria for approximately $3.5 billion, and divested its Henry Bath and Sons London Metals Exchange warehouse business in 2015. Bank of America retains a modest physical natural gas footprint primarily for client hedging support.

The Canadian banks (BMO Capital Markets, RBC Capital Markets, Scotiabank, and TD Securities) run substantial producer hedging desks for their Canadian and US E&P client base. The Canadian regulatory framework and the cross-border nature of the producer client base have allowed these desks to remain active in physical commodity hedging where US bank holding companies have wound down. Canadian bank desks are now the largest natural gas swap counterparties for North American small and mid-cap producers.

The shrinkage of the bank physical desks created the talent pool from which the multi-strategy hedge fund energy desks were built. The single largest cohort of senior gas traders moved from J. Aron, Morgan Stanley Commodities, and Bear Stearns Energy in stages from 2008 through 2020 into the natural-gas desks at Citadel, Millennium, Point72, and the energy specialist funds. The capital and the books migrated; the function did not disappear.

Inside the desk

A typical gas trading desk, whether at a bank, a multi-strategy fund, or a marketer, is organized into three functions that sit close enough to share a row.

Paper tradersrun the financial book. They split into four sub-roles. Henry Hub outright traders hold positions in NYMEX NG futures and OTC swaps, expressing views on the front month, the calendar strip, and the prompt year against fundamentals. Basis spread traders trade the differential between Henry Hub and a regional hub (Algonquin, Dom South, Waha, Sumas, AECO, Chicago Citygate, Houston Ship Channel) using ICE basis swaps and the OTC bilateral basis market; the basis book is where most of the desk’s alpha is generated, since the spreads price congestion and the front-month outright price is largely consensus. NGL traders run the propane, butane, ethane, isobutane, and natural gasoline strip out of Mont Belvieu, Conway, and the Gulf Coast export docks, often hedged with crude oil swaps (the propane-to-WTI percent-of-crude basis) or with Henry Hub (the ethane frac spread). Option traders run NYMEX NG and ICE basis options across the front year and the deferred strip, expressing volatility and skew views and hedging exotic structures the desk has written for clients. The four roles sit next to each other physically and read each other’s screens. They sit next to the power desk where the firm has one (electricity traders running PJM, ERCOT, NYISO, CAISO, ISO-NE locational marginal price contracts and capacity products, with the spark spread as the obvious cross-market connector) and to the coal desk where the firm still has one (a smaller and shrinking footprint covering API2 and Newcastle paper plus the residual US delivered-rail market, with the dark spread and the coal-to-gas switching boundary as the connector to the power and gas books).

Physical traders and schedulersrun the molecule. They hold the firm transportation contracts on the interstate pipelines, nominate volumes day by day on the Electronic Bulletin Board, post and lift capacity-release postings, manage imbalance penalties with the pipelines, and clear the daily delivery against the LDC and end-user customer book. Their time horizon is intraday and next-day. The schedulers also run the bidweek physical book, transacting the volume that anchors the next month’s Inside FERC index. The physical desk talks to the paper desk constantly because every physical position implies a paper hedge and every paper position has to be consistent with what the physical book can actually deliver.

Strategists and researchbuild the supply-and-demand model. The S&D modeler ingests pipeline scrape data at the receipt-and-delivery node level (Genscape, BTU Analytics, Wood Mackenzie, S&P Global Commodity Insights, and the open-source EBB nominations published by each pipeline), the European and US weather model runs and their ensemble outputs, LNG tanker AIS feeds for both export-terminal feedgas demand and overseas regasification arrivals, fundamental data from adjacent markets (wind speed forecasts and observed renewable generation by ISO, solar irradiance forecasts, coal stockpile levels at major delivery points, hydro reservoir levels in the Pacific Northwest and the Canadian shield), and the EIA weekly storage report. The model produces a balance sheet for the next 1, 7, 14, and 30 days and a probability-weighted view on the front-month futures fair value. The strategist’s output is what the paper traders read first thing each morning and what they read first when a model run releases. The research team is what differentiates a desk that prints alpha from a desk that prints volatility.

Hedge funds and specialist commodity traders

Multi-strategy hedge funds run the dominant share of the speculative gas book today. Citadel LLC operates one of the largest dedicated natural gas teams on the Street; Citadel Energy Marketing, founded in 2014, is one of the largest physical natural gas shippers in North America. Millennium Management runs a similarly large gas-and-power book. Point72 Asset Management, ExodusPoint Capital, Balyasny Asset Management, and Hudson Bay Capital all operate energy desks with material gas exposure.

Energy-specialist funds. Andurand Capital Management, founded by Pierre Andurand in 2013 and based in London, runs concentrated commodity-macro books across crude oil, natural gas, and broader energy. Statar Capital, founded by Ron Ozer in 2018 and based in Miami, is one of the largest dedicated natural gas funds. Goldfinch Partners is a Houston-based commodity-fundamental fund. Three Rivers Capital and Westbeck Capital round out the smaller specialist tier.

Power-and-gas-specialist funds. Helikon Investments, run out of London, is one of the longer-tenured power-and-gas-specialist funds. Saturn Investment Management is a smaller specialist focused on European and US gas-and-power.

The historical reference for the category is John Arnold’s Centaurus Advisors, the Houston-based natural gas hedge fund that ran from 2002 through 2012 with assets reaching approximately $5 billion at peak. Arnold closed the fund in 2012 and retired from active trading; many of the senior gas traders at the multi-strats and at Statar are direct or one-degree alumni of Centaurus.

Trading houses

The five large independent commodity trading houses are not US-headquartered. Vitol Group, headquartered in Geneva and Rotterdam, is the largest independent oil trader globally and has built a substantial LNG book over the last decade. Trafigura Group, headquartered in Singapore and Geneva, runs an integrated LNG and natural gas book. Mercuria Energy Group, headquartered in Geneva, runs the former JP Morgan physical commodities book it acquired in 2014. Gunvor Group, headquartered in Geneva, runs an LNG and refined-products business. Glencore plc (LSE: GLEN), headquartered in Baar, Switzerland, runs an LNG and natural gas book through its energy products division. The trading houses are the spot-cargo counterparty for most US LNG exports. Cheniere’s contract structure with Vitol, Shell, Trafigura, and the other large trading houses has them buying LNG cargoes free-on-board at the Sabine Pass or Corpus Christi loading dock and reselling delivered ex-ship into TTF-priced European or JKM-priced Asian markets.

Exchanges, clearinghouses, and price reporting

CME Group (NASDAQ: CME), through its New York Mercantile Exchange division, lists the Henry Hub Natural Gas Futures contract that has been the dominant benchmark since its Tues April 3, 1990 launch. The contract trades twelve consecutive monthly listings (and longer-dated annual listings out roughly twelve years), with physical delivery at the Henry Hub junction in Erath, Vermilion Parish, Louisiana. CME also lists Henry Hub Natural Gas Options, calendar spreads, and a basis-swap suite covering most US delivery points.

Intercontinental Exchange, Inc. (NYSE: ICE) lists a competing Henry Hub Natural Gas futures contract (the LD1 contract) financially settled to the NYMEX expiry, plus the broadest basis-swap suite of any exchange globally. ICE also lists the European Title Transfer Facility (TTF) gas contract, the Northwest European NBP gas contract, and the Asian JKM (Japan-Korea Marker) financial swap. ICE acquired the International Petroleum Exchange in 2001, the Climate Exchange in 2010, and Interactive Data in 2015, and operates ICE Endex (the European gas market operator headquartered in Amsterdam). The TTF futures contract is the primary European gas hedging instrument; JKM is published as an S&P Global Platts assessment and traded as financial swaps on ICE and CME.

Nodal Exchange, owned by EEX Group (which is in turn part of Deutsche Börse), is a smaller US exchange focused on power futures and basis-swap products.

Price-reporting agencies. S&P Global Commodity Insights (formerly S&P Global Platts) publishes Inside FERC’s Gas Market Report, Gas Daily, and the Bidweek price assessments for first-of-month index trades. Argus Media publishes Argus Natural Gas Americas, an alternative price-reporting service with growing share in basis assessment. Natural Gas Intelligence, a family-owned firm based in Sterling, Virginia, publishes the Bidweek and Spot Gas indices used by a substantial share of US physical commercial trades. ICE Index publishes basis assessments derived from cleared trade data. Bloomberg and LSEG (Refinitiv) distribute the underlying data.

The first-of-month index dynamic is structurally important to the US gas market. A substantial share of US physical commercial trades, particularly utility purchases and producer-marketer aggregations, settles against a “first of month” index price set during the last five business days of the prior month at each of fifty or so US delivery points. The first-of-month index is set by polling and by averaging cleared transactions at each location. The Gas Daily index, a separate daily series, is used for spot transactions. The combination of the monthly index and the daily Gas Daily series defines most of the US physical pricing infrastructure outside of the futures-cleared book.

Regulators and policy bodies

The Federal Energy Regulatory Commission, headquartered in Washington, regulates interstate natural gas pipelines, LNG terminals, and the wholesale natural gas market under the Natural Gas Act of 1938 and the Natural Gas Policy Act of 1978. FERC issues certificates of public convenience and necessity for new pipelines and LNG facilities, sets tariff rates for interstate transportation, and oversees market behavior under its anti-manipulation authority. FERC has five commissioners appointed by the President and confirmed by the Senate; no more than three may be from a single political party. The Pipeline and Hazardous Materials Safety Administration (PHMSA), within the Department of Transportation, regulates pipeline integrity, leak surveys, and line-break response.

The Department of Energy’s Office of Fossil Energy and Carbon Management authorizes LNG exports under Section 3 of the Natural Gas Act, distinguishing between exports to Free Trade Agreement countries (which are presumptively in the public interest under Section 3(c)) and exports to non-FTA countries (which require a public-interest determination). The DOE pause on new non-FTA LNG export authorizations announced in January 2024 and the subsequent litigation, partial lifting, and policy revisions has been a recurring policy story through 2024, 2025, and 2026. The Environmental Protection Agency regulates methane emissions from oil and gas operations under the New Source Performance Standards (subparts OOOO, OOOOa, OOOOb, and OOOOc), and the EPA Greenhouse Gas Reporting Program requires annual emissions reporting from large facilities.

State public utility commissions regulate intrastate gas distribution, retail rates, and intrastate pipelines that operate entirely within a single state. The Texas Railroad Commission, despite its historical name, is the state oil-and-gas regulator and also regulates intrastate gas pipelines in Texas. The California Public Utilities Commission, the New York Public Service Commission, and the Pennsylvania Public Utility Commission are among the most consequential state regulators by gas volume.

The Commodity Futures Trading Commission oversees natural gas futures trading on CME and ICE under the Commodity Exchange Act, sets position limits for the front-month and other contracts, and brings enforcement actions against market manipulation. The CFTC’s anti-manipulation authority overlaps in part with FERC’s anti-manipulation authority over the physical wholesale market; the two agencies signed two memoranda of understanding in January 2014 that define the respective enforcement boundaries.

Industry associations

The Interstate Natural Gas Association of America (INGAA), based in Washington, represents the interstate pipeline industry and publishes pipeline-engineering technical standards adopted across the industry by reference. The American Gas Association (AGA), also Washington-based, represents the US natural gas distribution utilities and publishes the AGA Reports on natural gas industry technical standards (notably AGA Report Number 3 on orifice metering, the standard reference for custody-transfer measurement). The American Petroleum Institute (API), Washington-based, is the broad oil-and-gas advocacy organization and publishes API Standards covering upstream and midstream operations. The American Exploration and Production Council (AXPC) represents the large-cap public independent producers. The Independent Petroleum Association of America (IPAA), based in Washington, represents the smaller independent producers. The Center for LNG, an industry coalition, represents the LNG export terminal operators and developers in policy discussions.

The technical standards published by INGAA, AGA, and API show up in pipeline-quality specs, custody-transfer metering, and equipment specifications throughout the rest of this book. A pipeline-quality specification of “1,030 Btu per cubic foot, water vapor not exceeding 7 pounds per million cubic feet, hydrogen sulfide not exceeding 0.25 grains per 100 cubic feet” comes directly from the AGA-INGAA cross-reference standards. The associations are not regulators; their work is the technical lingua franca that the regulators incorporate.

The molecule’s journey

A single molecule of methane drilled at a Marcellus wellhead in Greene County, Pennsylvania by Range Resources passes through nine identifiable categories on its way to combustion in a Tokyo gas-fired power plant. Range hires Patterson-UTI to drill the well and Halliburton to perform the slickwater frac. The producing well delivers raw gas through a small-diameter gathering line operated by MPLX (formerly MarkWest) to a cryogenic processing plant in southwestern Pennsylvania, where ethane and heavier components are removed and the residual methane is delivered to the Texas Eastern Pipeline (Enbridge) for interstate transport. A gas marketer, BP Energy Company, holds the firm transportation capacity from the Texas Eastern receipt point south to the Henry Hub delivery zone and schedules the day’s flow on the pipeline’s electronic bulletin board. The molecule passes through the Henry Hub junction; custody is documented at the AGA-3 metering station; a price is set against the NYMEX-cleared front-month settle. The molecule continues by Tennessee Gas Pipeline to Sabine Pass, where Cheniere Energy liquefies it into LNG. Vitol Group buys the cargo free-on-board at the loading dock at the JKM-linked spot price, charters an LNG carrier from Mitsui OSK Lines, and ships the cargo through the Strait of Malacca to a regasification terminal in Tokyo Bay. JERA, the joint venture between Tokyo Electric Power and Chubu Electric, buys the regasified molecule under a delivered ex-ship contract priced against JKM and burns it through a Mitsubishi Heavy Industries gas turbine to produce electricity. Every name in this chapter has a role in that journey.

Amaranth, September 14 to 21, 2006

A brief aside on the largest single-fund natural gas blowup in the history of the market.

Amaranth Advisors LLC was a Greenwich, Connecticut-based multi-strategy hedge fund founded by Nicholas Maounis in 2000. By mid-2006 the fund managed approximately $9.2 billion across credit, equities, convertible bonds, and energy. Brian Hunter, a Calgary-trained Canadian gas trader recruited from Deutsche Bank in 2004, ran the energy book and held a structurally large long-March-2007 short-April-2007 calendar-spread position on NYMEX Henry Hub futures, on the thesis that winter heating demand and a tight US storage picture would steepen the calendar spread before March expiry.

Through August and into September 2006, mild weather forecasts and ample storage injections compressed the spread Hunter had bet would steepen. By Wed September 13, 2006 the position was deeply underwater. Over five trading days from Thurs September 14 through Wed September 20, Amaranth lost approximately $6.6 billion, the largest single-fund loss in hedge fund history at the time. JPMorgan Chase and Citadel LLC partitioned the energy book in an emergency transfer over the weekend of September 21 and 22, 2006, with JPMorgan taking the natural gas physical and futures positions in exchange for fees and Citadel taking the remainder. The fund was wound down through Q4 2006.

The lesson for the market structure is in the partition. The book that brought down a $9 billion fund was absorbed in a weekend by two firms with the balance sheet to hold the position to expiry. Multi-strategy hedge funds and bank derivatives desks together now sit on the credit and capital that single-strategy funds did fifteen years ago.

The molecule moves through these categories from wellhead to burner tip, and every category carries a published price, a regulated tariff, or a cleared-trade reference somewhere along the chain. The next chapter, “Geology and Origins,” steps back from the corporate map to the rock map: the Devonian and Mississippian source rocks, the depositional environments, and the migration paths that put the methane underground in the first place.