Natural Gas Liquids: Physical

The NGL value chain from gas plant tap through Mont Belvieu fractionation, salt-cavern storage, NGL pipelines, export terminals at Morgan’s Point and Marcus Hook, and the petrochemical, residential, and gasoline-blending demand stack.

Energy Transfer placed the Mariner East 2 pipeline into commercial service on Sat Dec 29, 2018. The 20-inch line ran 350 miles east from the Houston processing complex in Washington County, Pennsylvania, across the Allegheny front, under the Susquehanna and Schuylkill rivers, through the Pennsylvania farmland of Lancaster and Chester counties, and into the Marcus Hook industrial complex on the Delaware River outside Philadelphia. The construction had taken three years, run a billion dollars over budget, faced fourteen separate sinkhole incidents in the Lancaster and Chester County karst belt, and absorbed criminal charges, civil penalties, and a procession of state administrative orders. The line started moving propane and butane in late December 2018; ethane service commenced in early 2019.

Marcus Hook itself sat on a 781-acre former Sunoco refinery site that Sunoco had idled in 2011 and that Energy Transfer had retooled, beginning in 2013, into the only US East Coast natural gas liquids export terminal. Storage caverns leached out of the 1,500-foot-deep salt formations underlying the site held the inbound propane, butane, and ethane in segregated cells. Two ship-loading docks on the Delaware River loaded LPG carriers bound for Northwest Europe and ethane carriers bound for INEOS Rafnes in Norway.

The first day of Mariner East 2 service moved roughly 275,000 barrels of mixed NGLs from the Marcellus wet core to Marcus Hook. The line connected the Appalachian wet portion of the Marcellus and Utica shales to the Atlantic basin in a way that had not existed in 2008. The chapter that follows is the physical infrastructure that makes that connection possible: the cryogenic recovery train at the gas plant, the Y-grade pipeline grid into Mont Belvieu and Marcus Hook, the fractionation columns that split the mixed liquid into five purity products, the salt-cavern storage that buffers seasonal demand, and the export terminals that load the molecules onto carriers bound for Asia and Europe.

The NGL Value Chain End-to-End

The NGL physical chain runs from wellhead to wet gas stream to gas processing plant to Y-grade pipeline to fractionation hub to purity-product pipeline to end user. Chapter 9 covered the gathering and processing layer in detail, including the cryogenic recovery train that produces Y-grade. This chapter picks up at the gas plant tail-gas and follows the molecule downstream through fractionation and into the demand market.

Y-grade is a single mixed liquid stream produced at the cryogenic plant. The composition by volume is typically 40 to 50 percent ethane, 25 to 35 percent propane, 10 to 15 percent butanes split between normal butane and isobutane, and 5 to 10 percent natural gasoline (pentanes and heavier). The exact composition varies by source basin. Marcellus wet-core Y-grade from the Houston, Sherwood, and Cadiz plants in Pennsylvania, West Virginia, and Ohio runs ethane-heavy because the underlying reservoir delivers a wet gas stream rich in ethane and lean in heavier components. Permian Y-grade from the Delaware and Midland sub-basins runs more evenly distributed because the reservoirs deliver a wider boiling-point range. Eagle Ford condensate-window Y-grade runs pentanes-plus heavy because the reservoir is on the borderline between gas and oil and the processed liquids skew toward the heavy end.

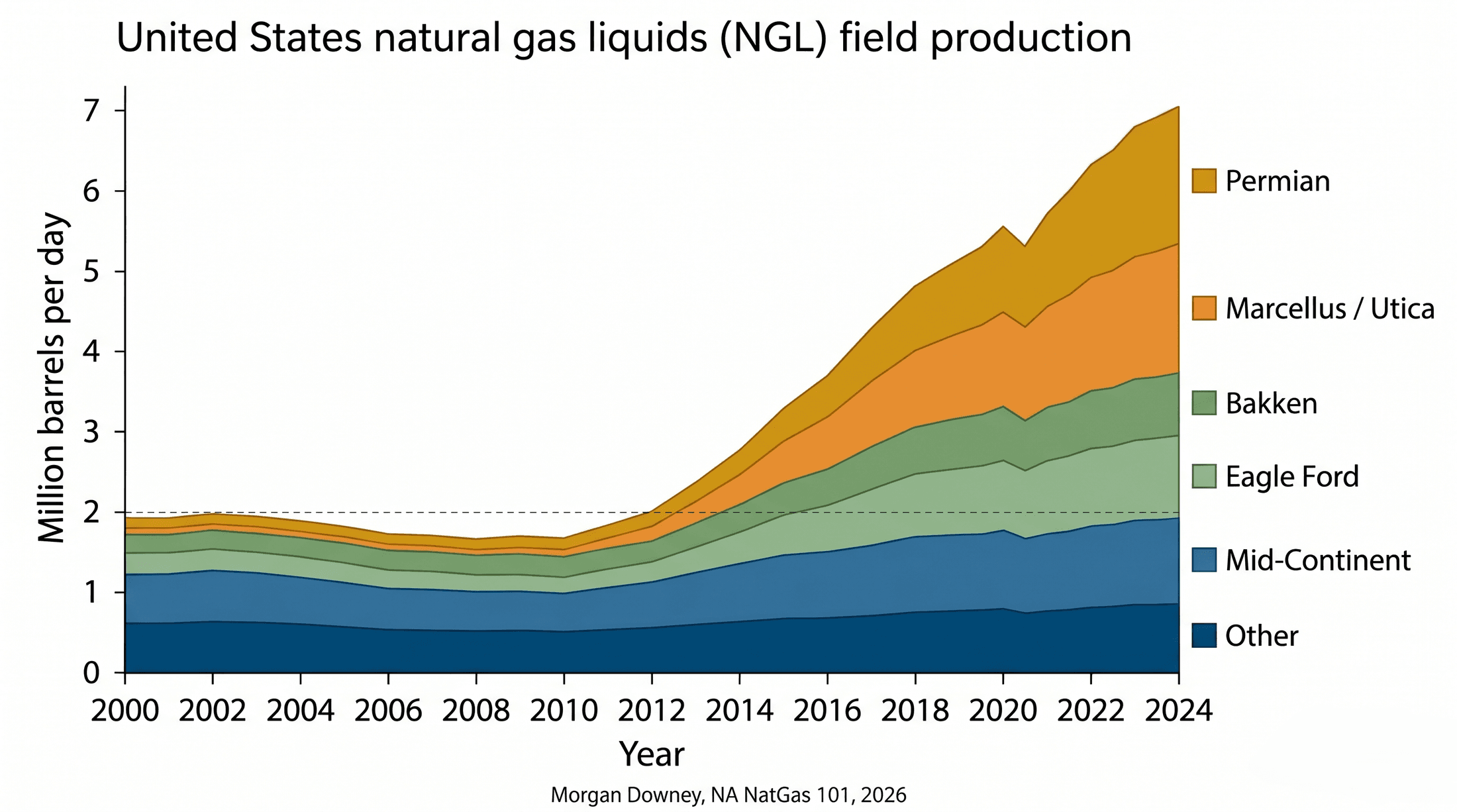

Total US NGL production reached roughly 7 million barrels per day in 2024, against roughly 2 million in 2010. The post-2010 growth came almost entirely from the Permian, the Marcellus, the Utica, the Bakken, and the Eagle Ford shale plays. The conventional NGL production base in the Mid-Continent, the Rockies, and the Gulf of Mexico shelf has been flat or declining over the same period. The shale revolution was not only a gas and oil revolution; it was also an NGL revolution that turned the United States from a net NGL importer at the end of the 2000s into the largest NGL exporter in the world by the mid-2020s.

The five purity products that fractionation produces from the Y-grade stream are ethane, propane, normal butane, isobutane, and natural gasoline. Each clears into a different end market. Ethane is a steam-cracker feedstock with a US Gulf Coast cracker fleet on one side and a small global cracker export market on the other. Propane is a residential heating fuel, a crop-drying fuel, an autogas, a petrochemical feedstock through propane dehydrogenation, and the largest single category of US LPG export. Normal butane is a winter gasoline blendstock and a steam-cracker feedstock for butadiene production. Isobutane is the alkylation feedstock at every major US refinery. Natural gasoline is a gasoline blendstock and the dominant diluent for Western Canadian heavy oil and bitumen blends. Each product carries its own price, its own forward curve, its own pipeline logistics, and its own seasonality. The fractionation train is the dividing line between the gas industry upstream and the petrochemical, refining, and consumer-fuel industries downstream.

Cryogenic Recovery and the Gas Plant Tail-Gas

The cryogenic recovery train at the gas plant is the unit operation covered in Chapter 9. The summary points relevant to this chapter follow.

Inlet wet gas enters the cold box, a brazed-aluminum heat-exchanger block sized for the plant capacity. The cold box cools the inlet stream by counter-current heat exchange against the residue methane stream and a refrigerant loop. The cooled gas then expands through a turbo-expander, dropping pressure from roughly 800 to 1,100 psig at the cold-box inlet to roughly 200 to 400 psig at the demethanizer column inlet, and dropping temperature to roughly minus 110 to minus 150 degrees Fahrenheit. The temperature drop condenses the C2-plus components into a liquid phase that falls into the demethanizer. Methane rises overhead and leaves the plant as residue gas to the interstate pipeline tap. The C2-plus liquid leaves the bottom of the demethanizer as Y-grade NGL, pumped to the NGL pipeline tap that runs to a fractionation hub.

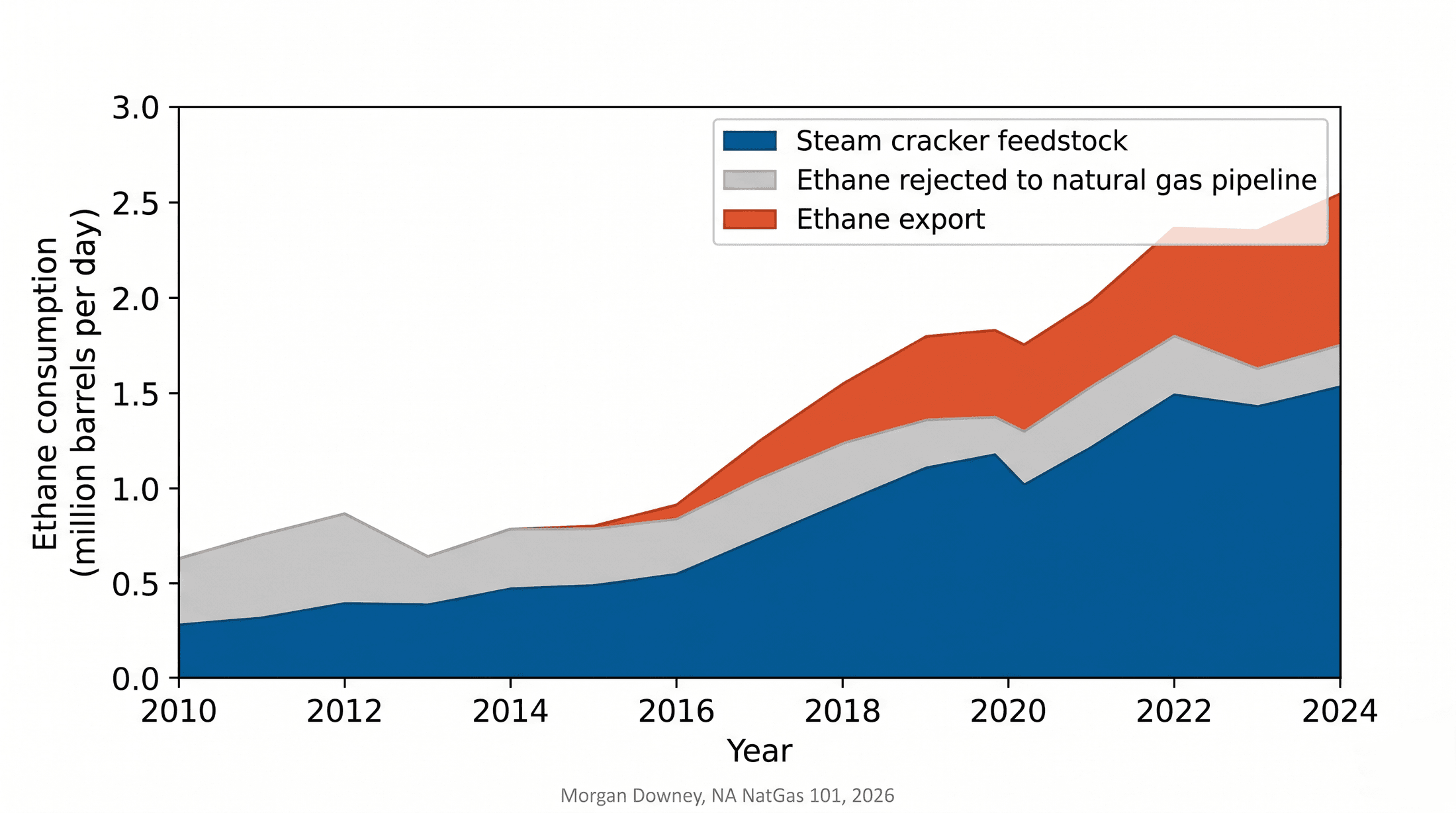

The recovery rate of ethane is the operator’s primary economic decision. In ethane-recovery mode, the plant runs the demethanizer at a low overhead temperature and captures roughly 90 percent of the ethane present in the inlet stream as a separated NGL. The recovered ethane leaves with the Y-grade and is sold as a purity ethane product after fractionation at Mont Belvieu. In ethane-rejection mode, the plant runs the demethanizer at a higher overhead temperature, allowing ethane to leave with the methane in the residue gas as heating-value contribution rather than as a separated NGL. The rejected ethane raises the heating value of the residue stream and is sold at the gas-equivalent price into the interstate pipeline. The plant produces less Y-grade volume but the residue gas is worth more on a per-MMBtu basis.

The choice between recovery and rejection is set by the frac spread, the per-MMBtu margin between Mont Belvieu purity ethane priced as a liquid and Henry Hub gas priced as the substitute heating-value outlet. When the spread is wide, recovery is the profitable choice. When the spread is narrow, rejection is the profitable choice. The frac spread is a topic of Chapter 19. The volume swing between fully recovered and partially rejected mode shifts US ethane production by roughly 200,000 to 400,000 barrels per day depending on price conditions and processing-plant operational flexibility. The swing is a structural feature of the US gas economy that does not exist in any other major producing basin in the world.

The plant ships the Y-grade by NGL pipeline. The dominant flow is south to Mont Belvieu through the Permian, Mid-Continent, and Rockies trunk systems, or south and east through the Marcellus and Utica trunk systems. A minority flow is east to Marcus Hook through the Mariner pipelines or north and east to Conway, Kansas, through the Bakken NGL Pipeline.

Fractionation at Mont Belvieu

The Y-grade enters a fractionation train at Mont Belvieu, in Chambers County, Texas, 30 miles east of Houston. Mont Belvieu sits above the Barbers Hill salt dome, a Jurassic-age halite intrusion roughly two miles in diameter that supports both the surface fractionation infrastructure and the subsurface storage caverns. Total Mont Belvieu fractionation capacity exceeds two million barrels per day across Enterprise Products Partners, Targa Resources, ONEOK, and Energy Transfer’s Lone Star NGL operating subsidiary, the four major operators in the cluster.

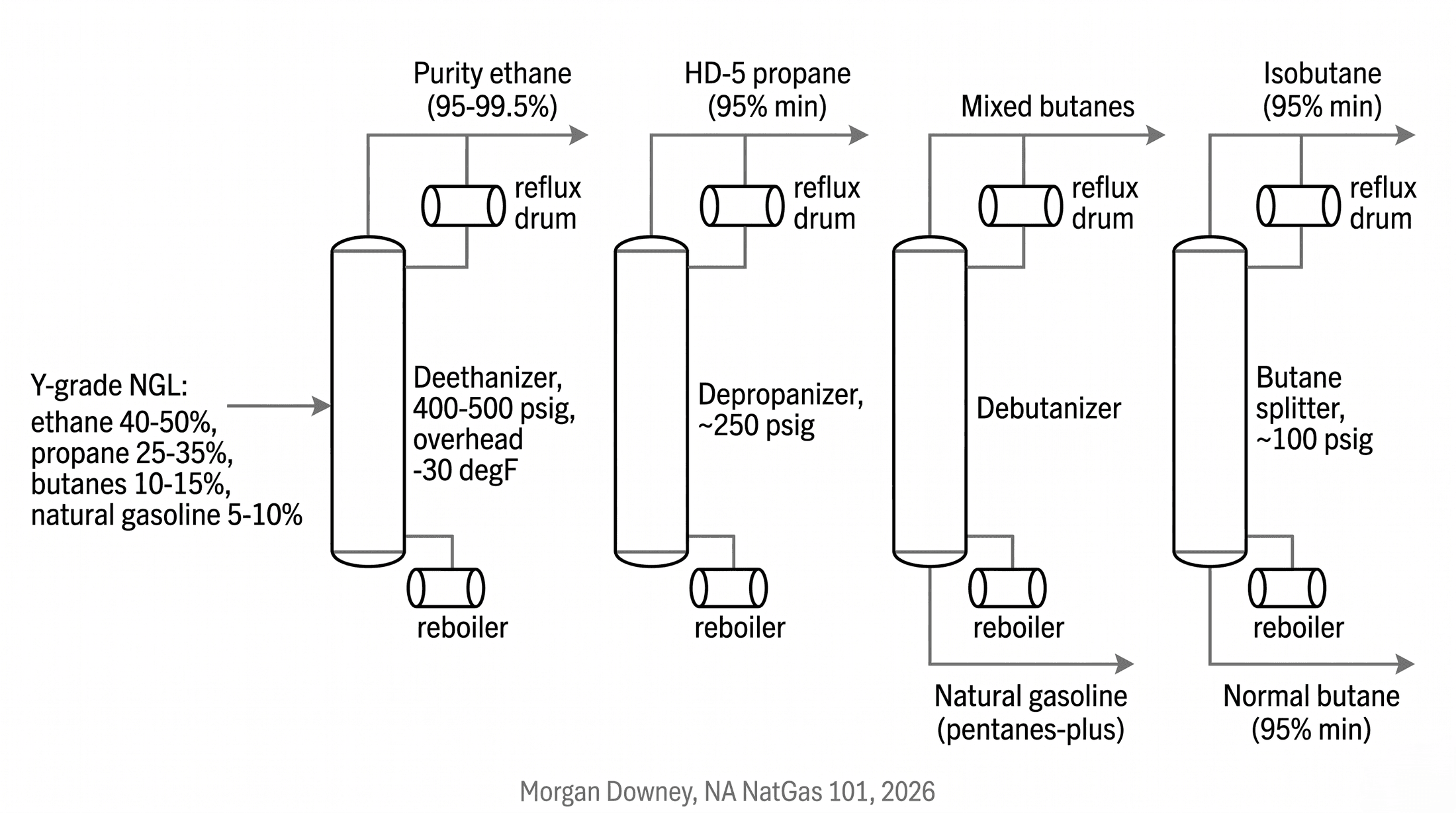

The fractionation train splits Y-grade by boiling point through a sequence of four distillation columns. Each column operates at a pressure and a temperature profile tuned to drive a single component overhead and the heavier components to the bottom.

The deethanizer is the first column. Y-grade enters the column at intermediate pressure, typically in the range of 400 to 500 psig, and ambient or slightly heated feed temperature. Ethane is the lightest component in the Y-grade stream and rises overhead. The column overhead operates at roughly minus 30 degrees Fahrenheit at the condenser outlet, the temperature at which the column reflux returns ethane to the top trays as a liquid while pure ethane vapor leaves the condenser as a product stream. The product stream is delivered as polymer-grade ethane (95 to 99.5 percent ethane content) or mid-grade ethane (90 to 95 percent), with the specification set by the downstream cracker buyer. The column bottoms (propane, butanes, and natural gasoline) feed the next column.

The depropanizer is the second column. The deethanizer bottoms enter the column at roughly 250 psig. Propane rises overhead and is condensed into a propane product stream meeting the GPA Midstream HD-5 specification, which requires 95 percent minimum propane content with strict limits on butanes and heavier components. HD-5 propane is the standard purity grade for the US LPG retail and petrochemical market. The depropanizer bottoms (mixed butanes and natural gasoline) feed the next column.

The debutanizer is the third column. The depropanizer bottoms enter the column at lower pressure than the depropanizer. Mixed butanes (combined normal butane and isobutane) rise overhead and the bottoms are pentanes-plus, recovered as natural gasoline. The natural gasoline is run-down to a stabilizer or directly to a storage tank for shipment to gasoline blending or to Western Canadian heavy-oil diluent service.

The butane splitter is the fourth column. Mixed butanes from the debutanizer overhead enter the column, typically at roughly 100 psig. Normal butane and isobutane separate by their narrow boiling-point difference: normal butane boils at roughly minus 0.5 degrees Celsius at standard pressure and isobutane boils at roughly minus 11.7 degrees Celsius. The closeness of the two boiling points means the butane splitter requires a tall column with a high reflux ratio and a substantial reboiler heat input to achieve the 95 percent minimum purity specification on each leg. Isobutane rises overhead because it is more volatile. Normal butane leaves as the bottom product.

Each column in the fractionation train operates with a reboiler at the bottom and a condenser at the top. The reboiler boils a portion of the column bottoms back up the column to provide vapor traffic. The condenser cools a portion of the overhead vapor back to liquid to provide reflux. The ratio of reflux to product (the reflux ratio) is the principal operating lever the operator uses to adjust product purity. A higher reflux ratio drives higher product purity at the cost of higher energy consumption and lower throughput. Modern Mont Belvieu fractionation trains run continuously and at design throughput, with periodic turnarounds for column inspection, tray cleaning, and condenser and reboiler maintenance.

The total fractionation footprint at Mont Belvieu is concentrated in two geographic clusters. The Enterprise Products Partners footprint sits on the eastern side of the city near the Barbers Hill cavern field and includes nine major fractionation trains as of the mid-2020s. The Targa Resources, ONEOK, and Energy Transfer Lone Star NGL footprints sit on the western and northern sides of the city, with their own train counts and storage cavern positions. The fractionation cluster is the price-discovery point for US NGL purity products. The chemistry that turned the wellhead stream into five separately tradable commodities is fixed. The fractionation columns at Mont Belvieu are where the trade actually clears.

Mont Belvieu Salt-Cavern Storage

The Barbers Hill salt dome supports approximately 100 million barrels of working NGL storage capacity in solution-mined salt caverns at depths of roughly 2,500 to 4,500 feet. The caverns are constructed and operated using the solution-mining and brine-cycling mechanics covered in Chapter 11 for natural gas storage. The mechanical principle is the same. Fresh water is injected through a borehole into the salt formation, the salt dissolves into brine, the brine is withdrawn, and the resulting cavern provides containment for stored hydrocarbons.

The mechanical differences between an NGL cavern and a natural gas cavern are operational rather than geological. NGL caverns operate at higher pressures because the stored product is a liquid (or a high-pressure liquid-vapor mix in the case of ethane) rather than a low-density gas. Cycling rates run higher because the seasonal and weekly demand swings on individual purity products are sharper than the swings on residential natural gas heating load. Propane caverns at Mont Belvieu and Conway are cycled 8 to 15 times per year at the most actively traded facilities, against 1 to 2 turns per year on a typical seasonal natural gas storage facility. Ethane caverns cycle at higher rates still, supplying the steady Gulf Coast cracker draw.

Each purity product has its own dedicated cavern fleet. Cross-contamination between products is operationally unacceptable because the downstream specification requires single-product purity. A propane cavern stores propane only. An ethane cavern stores ethane only. A butane cavern stores either normal butane or isobutane but not both. A natural gasoline cavern stores pentanes-plus only. The dedicated-cavern structure means the storage footprint at Mont Belvieu is segregated by product, with each operator running its own segregated cavern positions across the five products.

Propane caverns are the largest by working capacity and the most actively cycled. Residential heating draws across the Midwest and Northeast, crop-drying draws in October across the corn belt, and steady petrochemical and export draws all pull propane out of the Mont Belvieu and Conway storage complex. The seasonal pattern is sharpest at Conway, which serves the Mid-Continent and Midwest residential propane retail network and prices independently of Mont Belvieu during winter peaks. Ethane caverns are smaller per facility but high-deliverability, supplying the Gulf Coast steam cracker fleet on a near-continuous draw with limited seasonality. Butane caverns track the Reid Vapor Pressure-driven gasoline blending demand: high winter draw when butane can be blended into the gasoline pool at higher RVP specifications, low summer draw when the EPA RVP specifications exclude butane from the gasoline pool. Natural gasoline caverns track the bitumen-diluent and gasoline-blending markets with a seasonality that follows Western Canadian crude production rates.

The Conway, Kansas salt-cavern complex provides the secondary fractionation and storage hub for Mid-Continent NGL flows. Conway is principally operated by ONEOK on the back of legacy NGL pipeline assets that ONEOK acquired through the breakup of Mid-Continent gas pipeline systems in the 1990s and 2000s. Conway’s working capacity runs roughly 20 to 30 million barrels. The hub serves the Mid-Continent and Rockies producers as the inland alternative to the long Y-grade haul to Mont Belvieu, and the residential propane retail network across the upper Midwest as the seasonal supply source. Conway prices independently of Mont Belvieu during the residential heating peak and during regional logistical constraints.

The NGL Pipeline Grid

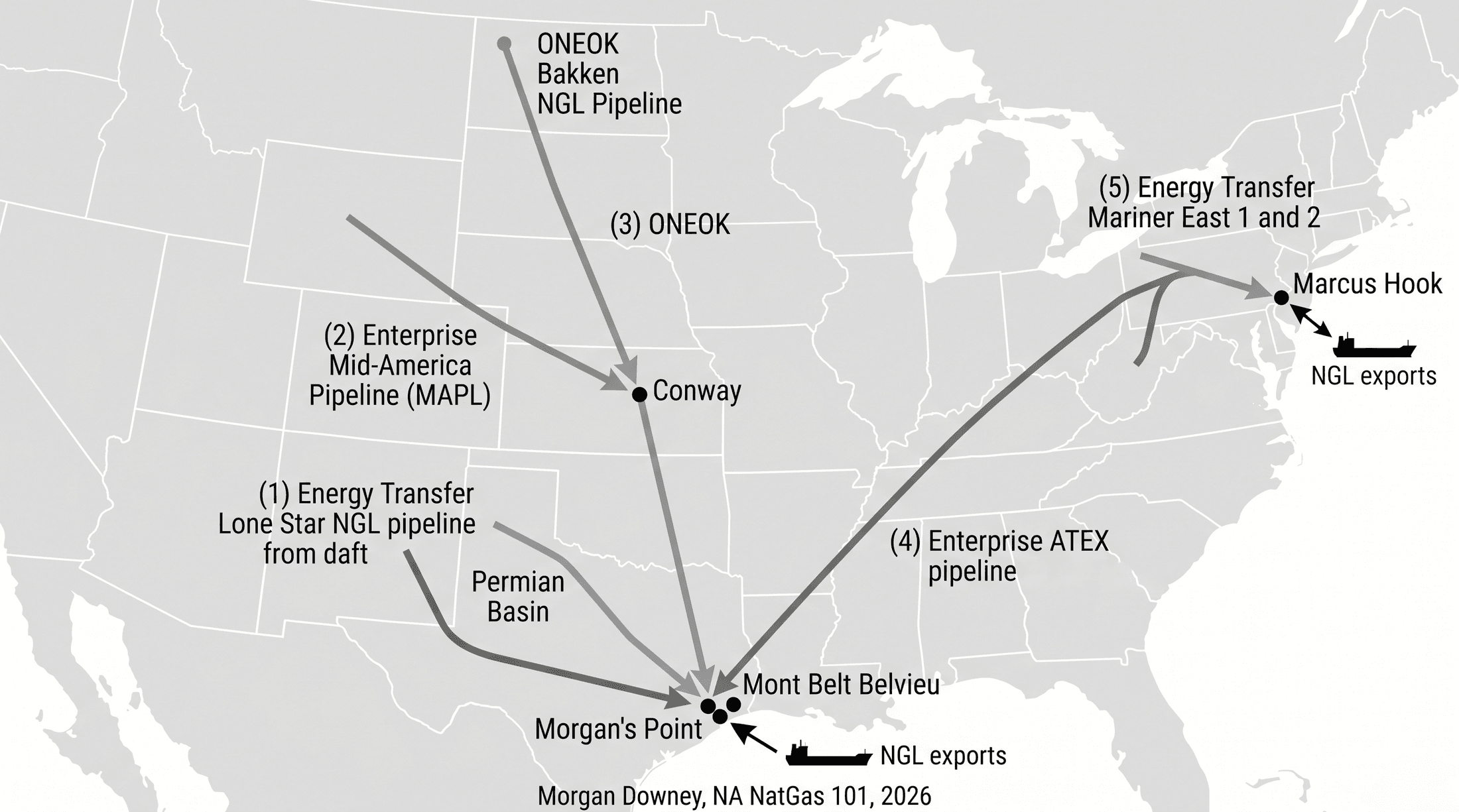

The Y-grade NGL pipeline system that brings raw NGLs from gas plants to Mont Belvieu and Conway is built around four major trunk systems operated by four midstream companies.

Energy Transfer’s Lone Star NGL pipeline complex carries Permian and Mid-Continent Y-grade south to Mont Belvieu. The legacy assets in this complex include the former Regency NGL system and elements of the former Sunoco Logistics NGL infrastructure that Energy Transfer acquired in 2017. The Lone Star system is the largest single Y-grade trunk into Mont Belvieu by volume.

Enterprise Products Partners’ Mid-America Pipeline (MAPL) and the Enterprise NGL pipeline complex bring Permian, Mid-Continent, and Rockies Y-grade to Mont Belvieu and the surrounding Texas Gulf Coast. The MAPL system, originally built in the 1960s to move Rocky Mountain NGLs to the Mid-Continent and reversed and expanded over time, runs from western Wyoming through the Mid-Continent to Mont Belvieu. Enterprise also operates the Appalachia-to-Texas (ATEX) ethane pipeline, which runs in the opposite direction of the dominant Y-grade flow: from the Marcellus and Utica wet core to Mont Belvieu, providing supplementary Marcellus and Utica ethane access to the Gulf Coast cracker fleet.

ONEOK operates the Bakken NGL Pipeline, the Mid-Continent NGL system, and the Conway hub. The Bakken NGL Pipeline runs from western North Dakota through the Mid-Continent to Conway and onward to Mont Belvieu, providing the primary Bakken Y-grade takeaway. ONEOK’s 2023 acquisition of Magellan Midstream Partners combined the legacy ONEOK NGL system with Magellan’s refined-product pipeline footprint under a single midstream operator with both NGL and refined-product logistics positions.

MPLX operates the legacy MarkWest gathering and Y-grade collection system in southwestern Pennsylvania, the West Virginia northern panhandle, and eastern Ohio. The Y-grade collected at the MPLX plants in Houston, Sherwood, and Cadiz feeds eastward into the Energy Transfer Mariner East system or south and west into the MPLX-Enterprise interconnects that move Marcellus and Utica Y-grade to Mont Belvieu through the ATEX pipeline and other connecting infrastructure. MPLX is Marathon Petroleum’s midstream subsidiary, formed in 2012 and expanded through the 2015 acquisition of MarkWest Energy Partners.

Once Y-grade reaches Mont Belvieu, purity-product pipelines distribute the fractionated NGLs to end markets. Ethane and ethylene pipelines from Mont Belvieu to the Houston Ship Channel petrochemical complex deliver ethane to the Gulf Coast steam cracker fleet at Cedar Bayou, Channelview, La Porte, Pasadena, and Sweeny, and supply the export ethane terminal at Morgan’s Point. Propane pipelines deliver HD-5 propane to inland propane terminals across the Mid-Continent and Southeast for retail distribution and to the Gulf Coast LPG export terminals. Refinery pipelines deliver isobutane to the alkylation units at Texas, Louisiana, and Oklahoma refineries, and deliver normal butane to gasoline blending terminals in winter months when RVP specifications allow.

The Energy Transfer Mariner East 1 (an 8-inch line repurposed from the original Sunoco Logistics liquid petroleum products system) and Mariner East 2 (the 20-inch line placed in service in December 2018) deliver Marcellus and Utica NGLs east to Marcus Hook on the Delaware River. Combined Mariner East 1 and 2 capacity exceeds 400,000 barrels per day across the propane, butane, and ethane streams. The Mariner East system is the only NGL trunk that delivers Appalachian liquids directly to an Atlantic export terminal. Every other major US NGL export point sits on the Texas or Louisiana Gulf Coast.

Export Terminals: Morgan’s Point, Marcus Hook, and the Global LPG Trade

The Enterprise Hydrocarbons Terminal at Morgan’s Point on the Houston Ship Channel is the largest US NGL export facility. The terminal runs multiple loading docks for LPG (propane and butanes), ethane, and natural gasoline, with separate cargo systems that prevent cross-contamination between products. Combined US NGL exports through the Gulf Coast and East Coast terminals reached roughly 2.5 to 3 million barrels per day in 2024 across LPG, ethane, and natural gasoline, against effectively zero US NGL exports in 2010.

The Energy Transfer Marcus Hook complex on the Delaware River, built on the former Sunoco refinery site outside Philadelphia, is the second-largest US NGL export terminal and the only one on the East Coast. Marcus Hook exports propane, butane, and ethane to Northwest Europe, with the longer Atlantic crossing producing different cargo economics from the Gulf Coast terminals. The Targa Galena Park terminal on the Houston Ship Channel exports propane and butane primarily. The Phillips 66 Freeport LPG terminal exports propane and natural gasoline. Smaller export operations run at the Energy Transfer Nederland terminal and the Enterprise Beaumont terminal on the upper Texas coast. The Texas Gulf Coast terminal cluster, taken together, accounts for the dominant share of US LPG and ethane exports.

US LPG exports go primarily to Asia (China, Japan, Korea, and India for cooking, transportation fuel, and petrochemical feedstock), to Northwest Europe (the Antwerp and Rotterdam petrochemical and retail LPG complex), and to Latin America (Brazil, Mexico, and the Caribbean) as the third major destination. Asian buyers run the largest aggregate volume on the back of substantial residential and commercial LPG demand, the propane dehydrogenation fleet in China that converts US-sourced propane into propylene for the Chinese petrochemical industry, and steam crackers in Japan and Korea that take propane as a swing feedstock against naphtha. European LPG demand is principally retail residential and small commercial heating, with a smaller petrochemical feedstock component. Latin American demand is principally retail residential cooking gas in markets where piped natural gas distribution is limited and the LPG retail network covers the substitution gap.

US ethane exports go to a dedicated set of long-term cracker buyers. INEOS Rafnes in Norway, supplied via Marcus Hook, was the first international US ethane buyer. Borealis Stenungsund in Sweden, supplied via Marcus Hook, took early ethane cargoes alongside INEOS. Reliance Industries Dahej in Gujarat, India, supplied via Morgan’s Point, took the first US ethane cargo to Asia in 2017 under a 2014 long-term sale and purchase agreement with Enterprise Products Partners. SP Chemicals at Taixing and Wanhua Chemical at Yantai, both in China, take US ethane under long-term contracts to feed dedicated ethane crackers built in the late 2010s and early 2020s. The SK Geocentric NCC and the Yeochon NCC complexes in South Korea take US ethane as a swing feedstock alongside naphtha.

Each ethane export buyer holds a long-term sale and purchase agreement with Enterprise Products Partners or Energy Transfer for 15 to 25 years, with pricing structured against Mont Belvieu purity ethane plus a fixed shipping fee that covers the dedicated ethane carrier service. The dedicated ethane carrier fleet, principally Very Large Ethane Carriers (VLECs) of 87,000 to 99,000 cubic meters capacity, was built specifically to serve the US ethane export trade and operates against the long-term contracts. Without the long-term commercial commitment, the carrier fleet does not exist; without the carrier fleet, the export trade does not exist. The two were built together.

The Five Purity Products and the Demand Stack

Each of the five purity products fractionated at Mont Belvieu serves a distinct demand market with its own seasonality, price drivers, and competing substitutes.

Ethane. The specification range covers polymer-grade ethane at 95 to 99.5 percent ethane content and mid-grade ethane at 90 to 95 percent. The dominant demand is feedstock to ethylene production through steam cracking. The US Gulf Coast steam cracker fleet, concentrated in the Houston, Lake Charles, and Corpus Christi clusters, consumes roughly 1.5 million barrels per day of ethane at full utilization. Ethane export adds another 600,000 to 800,000 barrels per day to total US ethane demand. The competing feedstock is naphtha, the conventional global cracker feedstock derived from crude oil refining. The ethane-versus-naphtha switching decision sets the marginal feedstock for the global cracker fleet outside the United States and is the topic of Chapter 21.

Propane. The specification is HD-5 (95 percent minimum propane content). Demand is split across residential and commercial space heating, crop drying, transportation fuel, petrochemical feedstock, and LPG export. Total US propane demand is roughly 1.4 to 1.6 million barrels per day. The seasonal swing is sharp. Residential and commercial heating demand peaks in January and February across the Northeast, the upper Midwest, and the Mountain West rural areas where propane is the dominant heating fuel. Crop-drying demand peaks in October across the corn belt during the autumn corn harvest. Transportation fuel (autogas for light vehicles and forklift propane in industrial applications) is roughly steady year-round. Petrochemical feedstock demand through propane dehydrogenation (PDH) at Houston and upper Texas coast units is steady year-round. LPG export is steady year-round with a seasonal tilt toward Northern Hemisphere winter heating demand at the Asian and European destinations. The competing fuel in the residential Northeast is heating oil (No. 2 fuel oil), and the propane-versus-heating-oil arbitrage is the topic of Chapter 21.

Normal butane. The specification is 95 percent minimum normal butane. Demand is split across gasoline blending in winter months when Reid Vapor Pressure regulations allow, butadiene production via steam cracking at the Texas and Louisiana butadiene units, and isomerization feedstock at refinery isomerization units that convert normal butane to isobutane to expand the alkylation feedstock pool. The seasonal gasoline-blending pattern is sharp. EPA Reid Vapor Pressure specifications limit the volatility of summer gasoline to roughly 7.8 or 9.0 psi RVP depending on region, which excludes butane (RVP near 52 psi as a pure component) from summer gasoline blending. Winter RVP specifications relax to 13 to 15 psi, allowing butane to be blended into the gasoline pool at substantial volumes. The structural effect is that butane caverns at Mont Belvieu fill through summer and draw down through winter as butane moves into the winter gasoline pool.

Isobutane. The specification is 95 percent minimum isobutane. The dominant demand is alkylation feedstock at refineries for high-octane gasoline blendstock production. The alkylation unit at every major US refinery uses isobutane plus light olefins (propylene and butylenes from the FCC unit) to produce alkylate, the highest-octane gasoline blending component in the conventional refinery gasoline pool. Total US refinery isobutane demand for alkylation runs in the range of 200,000 to 300,000 barrels per day, with refinery captive isobutane production through butane isomerization supplying part of the demand and Mont Belvieu purchase volumes supplying the balance. Legacy demand for isobutane in MTBE manufacture collapsed in the early-to-mid 2000s as state-level bans (California 2003, New York and Connecticut 2004) and the loss of federal Reformulated Gasoline oxygenate liability protection in the 2005 Energy Policy Act phased MTBE out of the US gasoline pool; alkylation demand has been the dominant outlet since.

Natural gasoline. The specification is pentanes-plus, typically 75 to 85 octane and high vapor pressure (Reid Vapor Pressure in the range of 9 to 14 psi). Demand is split across gasoline blending for octane and vapor pressure adjustment, and diluent for Western Canadian heavy oil and bitumen blends pipelined to US Gulf Coast and Midwest refineries. The Canadian heavy-oil diluent demand is the largest single non-domestic-blending outlet for US natural gasoline. Diluent volumes move by rail and pipeline from Mont Belvieu and Conway to Edmonton and Hardisty in Alberta, where the diluent is blended with bitumen and heavy oil to produce dilbit (diluted bitumen) and synbit (synthetic bitumen blend) that meets pipeline viscosity specifications for shipment south to the US Gulf Coast and Midwest. The natural gasoline market connects the US shale economy to the Canadian heavy oil sands economy in a feedback loop: US shale produces the diluent that allows Canadian bitumen to flow south, and the Canadian bitumen flowing south provides feedstock for US Gulf Coast refineries that produce the gasoline pool that consumes the natural gasoline as a blendstock.

The First US Ethane Export Cargo, March 2016

The JS INEOS Insight loaded ethane at Marcus Hook on Wed Mar 9, 2016, and sailed for INEOS Rafnes in Norway. The 27,500-cubic-meter Multi-Gas Carrier was the first vessel in a fleet INEOS had commissioned specifically to move US shale ethane across the Atlantic to its Norwegian cracker. The cargo was the first US ethane export in the country’s commercial history. The United States had been a net ethane importer through most of the 2000s, with limited domestic production beyond what Gulf Coast crackers could absorb and no infrastructure to move the molecule overseas.

The transformation between 2010 and 2016 had been engineered, not accidental. Range Resources and the early Marcellus producers had drilled the wet core. MarkWest, MPLX, and the rest of the Appalachian midstream segment had built the cryogenic recovery and the Y-grade collection. Energy Transfer (and its Sunoco Logistics predecessor) had retooled the former Sunoco refinery site at Marcus Hook into a deepwater export terminal. INEOS had financed the dedicated ethane carrier fleet against a 15-year sale and purchase agreement with the US supplier. The supply chain was built piece by piece in a deliberate sequence, and the first cargo was the first cash flow at the end of it.

Reliance Industries took the first US ethane cargo to Asia in late 2016 or early 2017 at its Dahej terminal in Gujarat, India, opening the Asian leg of the trade. The remaining Asian and European buyers followed over the next several years. By 2024 the US was exporting roughly 700,000 barrels per day of ethane across the dedicated VLEC fleet, against zero in March 2016. The first cargo set the precedent that the rest of the trade was built on.

Chapter 19 picks up at the price layer. Mont Belvieu purity ethane, HD-5 propane, normal butane, isobutane, and natural gasoline each clear into separate forward markets, against a stack of substitutes that sets the floor and ceiling on each price.