Gathering and Processing

Removing impurities, separating NGLs, the cryogenic plant, the amine sweetener, the dehydrator, and the path from wellhead to interstate pipeline tap.

Mont Belvieu sits 30 miles east of Houston in Chambers County, Texas. The 2020 census put the city’s population at 7,602. Beneath those few square miles of pine and pasture sits the Barbers Hill salt dome, a Jurassic-age halite intrusion roughly two miles in diameter, into which operators have leached out hundreds of caverns to store natural gas liquids. Above the dome sits the largest concentration of NGL fractionation capacity in the world. Enterprise Products Partners runs a complex of fractionation trains there. Targa Resources runs another. ONEOK runs another. Energy Transfer runs another. Total fractionation capacity at Mont Belvieu exceeds two million barrels per day across the operators, and the underlying salt-cavern storage exceeds 100 million barrels of working capacity.

The gas that arrives at Mont Belvieu does not arrive as gas. It arrives as a mixed liquid called Y-grade, pumped down from processing plants in the Permian, the Eagle Ford, the Marcellus, and the Bakken through long-haul NGL pipelines. The fractionation trains split the Y-grade into ethane, propane, normal butane, isobutane, and natural gasoline. The five purity products leave Mont Belvieu by pipeline to Gulf Coast steam crackers, by pipeline to refineries, by ship from Enterprise Hydrocarbons Terminal at Morgan’s Point on the Houston Ship Channel, and by truck and rail to inland customers.

The geographic concentration is the story. The infrastructure that makes a Marcellus dry-gas wellhead pad in Susquehanna County deliverable as ethylene feedstock to a Belgian cracker runs through this one Texas township. Chapter 9 starts at the wellhead the producer hands off to the midstream operator and ends at the fractionation tower that turns the wet portion of the wellhead stream into five separately tradable commodities.

Gathering: From Wellhead to Plant

The first piece of midstream infrastructure begins where the production tree ends. Immediately downstream of the wellhead a three-phase separator splits the produced fluid into gas, liquid hydrocarbon, and produced water. The separator sits on the pad, sized for the expected production rate, and runs at a back-pressure that depends on the gathering system it feeds into. Gas leaves the top of the separator. Condensate or oil drops to a stock tank or a heater treater. Produced water drops to a holding tank that is trucked or piped to a saltwater disposal well. The handoff from the producer to the gathering company happens at the meter run downstream of the separator, where flow is measured to a custody-transfer standard for royalty and severance-tax accounting.

Gathering systems run in two general configurations. A low-pressure system collects gas from multiple wells through small-diameter pipe, typically 4 to 12 inches in nominal diameter, into a gathering compressor station that raises the pressure to feed a larger trunk line running to the processing plant. The compressor stations are diesel- or electric-driven reciprocating or screw compressors, sized for the field’s peak gas rate, and add 200 to 800 psig of discharge pressure to the gathered stream depending on the trunk-line pressure they must overcome. A high-pressure system skips the first compression stage where wellhead flowing pressure is high enough to push the gas directly into the trunk line. Most Marcellus dry-gas pads in the Susquehanna County core run high-pressure gathering for the first several years of well life, then convert to compressed gathering as wellhead pressure declines into the depletion phase.

Pipe metallurgy and right-of-way mechanics constrain the system. Buried steel pipe is the standard, X42 or X52 grade, coated for corrosion protection and laid in trenched right-of-way. The right-of-way is acquired from surface owners under easement agreements that compensate the surface owner for the use of the land, the temporary disturbance during construction, and the permanent restriction on building over the line. Pennsylvania, Texas, and Louisiana each handle the easement-versus-eminent-domain framework differently, and gathering operators in some states cannot exercise eminent domain on a single-producer gathering line the way an interstate pipeline can on its FERC-jurisdictional infrastructure.

Operations run on SCADA. Each gathering compressor station and each major valve on the trunk reports flowing pressure, temperature, and flow rate back to a central operations center, often hundreds of miles away. A field operator drives the right-of-way weekly to walk the trunk and inspect the compressor stations, and the SCADA system catches deviations between the field visits.

The commercial structure splits two ways. Operator-owned gathering keeps the gathering system on the producer’s balance sheet, which preserves operational control and captures the gathering margin internally. Third-party midstream gathering, more common in the modern shale era, transfers the gathering capital to a midstream company under a long-term gathering agreement. The producer dedicates production from its acreage to the midstream company for a contract term of 10 to 20 years, and the midstream company builds and operates the gathering system in exchange for per-Mcf gathering fees and acreage dedication. The split between the two structures has shifted toward third-party gathering since 2010 as midstream MLPs and infrastructure investors have provided the capital that producers preferred to allocate to drilling instead.

The Processing Plant: Inlet to Outlet

The processing plant takes raw wet gas from the gathering trunk and produces two outputs. A residue methane stream that meets the receiving pipeline’s tariff specifications and goes to the interstate pipeline tap. A liquids stream that goes by NGL pipeline to a fractionation hub. The unit operations sit in a fixed sequence dictated by chemistry and thermodynamics. Each unit removes one impurity or separates one fraction, and the stream that leaves each unit is the inlet stream to the next.

Inlet receiving begins with a slug catcher. The gathering trunk delivers gas with intermittent slugs of liquid that have accumulated at low points in the pipe and surge through the line during pressure or flow transients. The slug catcher is either a finger-style vessel array or a horizontal separator, sized to absorb the largest expected slug volume without flooding downstream equipment. The gas continues through an inlet separator that drops out free water and condensate before the gas enters the treatment train.

Amine sweetening removes hydrogen sulfide and carbon dioxide. The gas flows up through an absorber column counter-current to a circulating amine solvent, typically monoethanolamine, diethanolamine, or methyldiethanolamine in aqueous solution at concentrations of 15 to 50 weight percent. The amine absorbs H2S and CO2 chemically. The treated gas leaves the top of the absorber. The loaded amine leaves the bottom and flows to a stripper column where heat input regenerates the solvent and releases the absorbed acid gases overhead. The acid-gas stream goes to a Claus sulfur-recovery unit when the H2S volume justifies the unit, or to a thermal oxidizer when it does not. MDEA has displaced MEA and DEA at most modern plants because MDEA is more selective for H2S over CO2, requires less regeneration energy, and degrades less in service.

Dehydration removes water. Bulk water removal happens in a triethylene glycol contactor, the same counter-current column-and-stripper architecture as the amine unit but with TEG instead of amine. TEG dries the gas to roughly 7 pounds of water per million standard cubic feet, the standard pipeline-tariff specification, but not below that level. Plants that feed cryogenic recovery downstream cannot tolerate that residual water because at minus 110 degrees Fahrenheit it freezes and plugs heat exchangers and the demethanizer column. Those plants run a deeper drying step on molecular sieves: zeolite beds with a pore size matched to the water molecule, regenerated periodically by hot dry gas. Molecular-sieve outlet water specifications are below 0.1 ppmv, far below the threshold for cryogenic operation.

Mercury removal is a small unit by volume but a critical one for downstream equipment integrity. Trace mercury attacks brazed-aluminum cryogenic heat exchangers by amalgamating with the aluminum and weakening the joints. A bed of sulfur-impregnated activated carbon adsorbs mercury to below 0.01 micrograms per cubic meter and is sized for years of service before the bed is changed out. Marcellus and Haynesville inlet gas typically carries low mercury and the bed is conservatively oversized; some Asia-Pacific gas streams carry mercury at concentrations that would make US bed-life economics painful.

Cryogenic recovery is where the NGL separation happens. The dried, sweetened, mercury-stripped gas enters the cold box, a brazed-aluminum heat-exchanger block in which the inlet gas is cooled by counter-current exchange against the residue methane stream and a refrigerant stream. The cooled gas then expands through a turbo-expander, a high-speed turbine that drops the gas from inlet pressure of roughly 800 to 1,100 psig down to a demethanizer pressure of 200 to 400 psig in a single stage. The expansion drops the temperature to roughly minus 110 to minus 150 degrees Fahrenheit at the cold-box outlet. The temperature drop condenses the C2-plus components into a liquid phase that drops into the demethanizer column. The work the expanding gas performs against the turbine is recovered as shaft work and used to drive a recompressor that boosts the residue gas back to pipeline pressure on the warm side of the cold box.

The demethanizer column is the separation device. The condensed liquid feed enters near the top of the column. Methane rises overhead as a gas, joins the warmed residue stream from the cold-box exchanger, and leaves the plant as residue gas to the pipeline tap. Ethane and heavier components fall to the bottom, are reboiled to drive remaining methane back up the column, and leave the column as a Y-grade NGL stream that exits the plant by NGL pipeline. The column operates at the pressure set by the turbo-expander discharge, with reflux and reboil controlled to hold the methane content of the Y-grade below the spec the downstream fractionator will accept. Modern cryogenic recovery is a settled technology. The first generation of turbo-expander cryogenic plants commercialized in the 1970s replaced refrigerated absorption units and lean-oil units that recovered NGLs less efficiently and at higher operating cost.

NGL Fractionation and Mont Belvieu

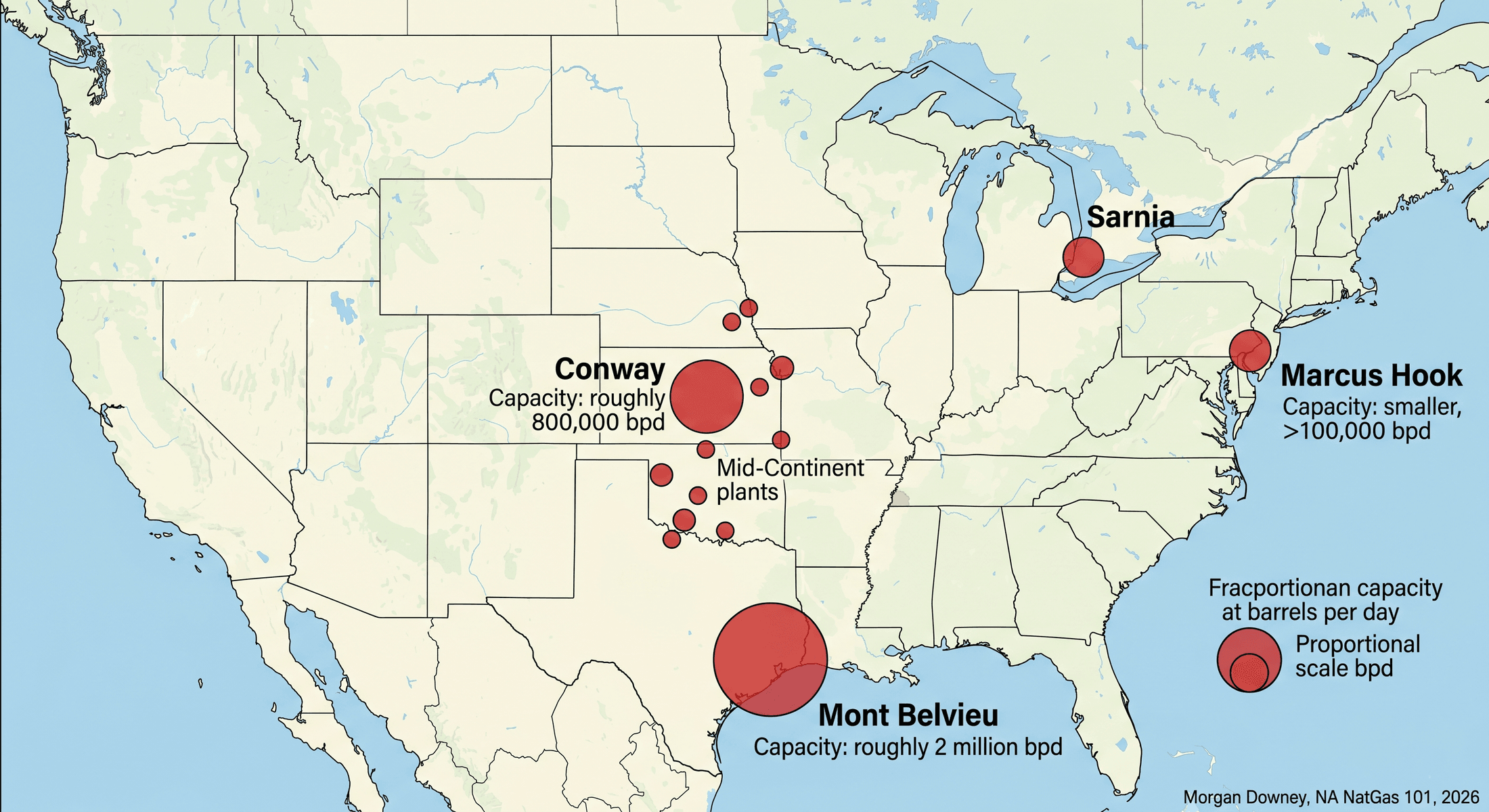

The Y-grade NGL leaves the processing plant as a single mixed liquid and travels by pipeline to a fractionation hub. The Mid-Continent and Permian Y-grade flows travel south and east through the Enterprise, ONEOK, and Energy Transfer NGL pipeline systems to Mont Belvieu and the broader Texas Gulf Coast fractionation cluster. Marcellus and Utica Y-grade flows travel west and south through the MPLX and Energy Transfer Mariner systems either to Mont Belvieu or to the Marcus Hook export and fractionation complex on the Delaware River outside Philadelphia. Bakken Y-grade flows travel south through the ONEOK Bakken NGL Pipeline to Conway in central Kansas and onward to Mont Belvieu.

Mont Belvieu is the canonical hub. Roughly 90 percent of US ethane fractionation capacity sits in Mont Belvieu and the immediately adjacent Texas Gulf Coast cluster. Total fractionation capacity across all Mont Belvieu operators exceeds two million barrels per day. The underlying Barbers Hill salt dome supports cavern storage of NGLs at high pressure and at low capital cost per barrel, with total working storage exceeding 100 million barrels across Enterprise, Targa, and the smaller operators. The combination of fractionation capacity, storage capacity, and dock access through the Houston Ship Channel and adjacent terminals makes Mont Belvieu the price-discovery point for US NGL purity products.

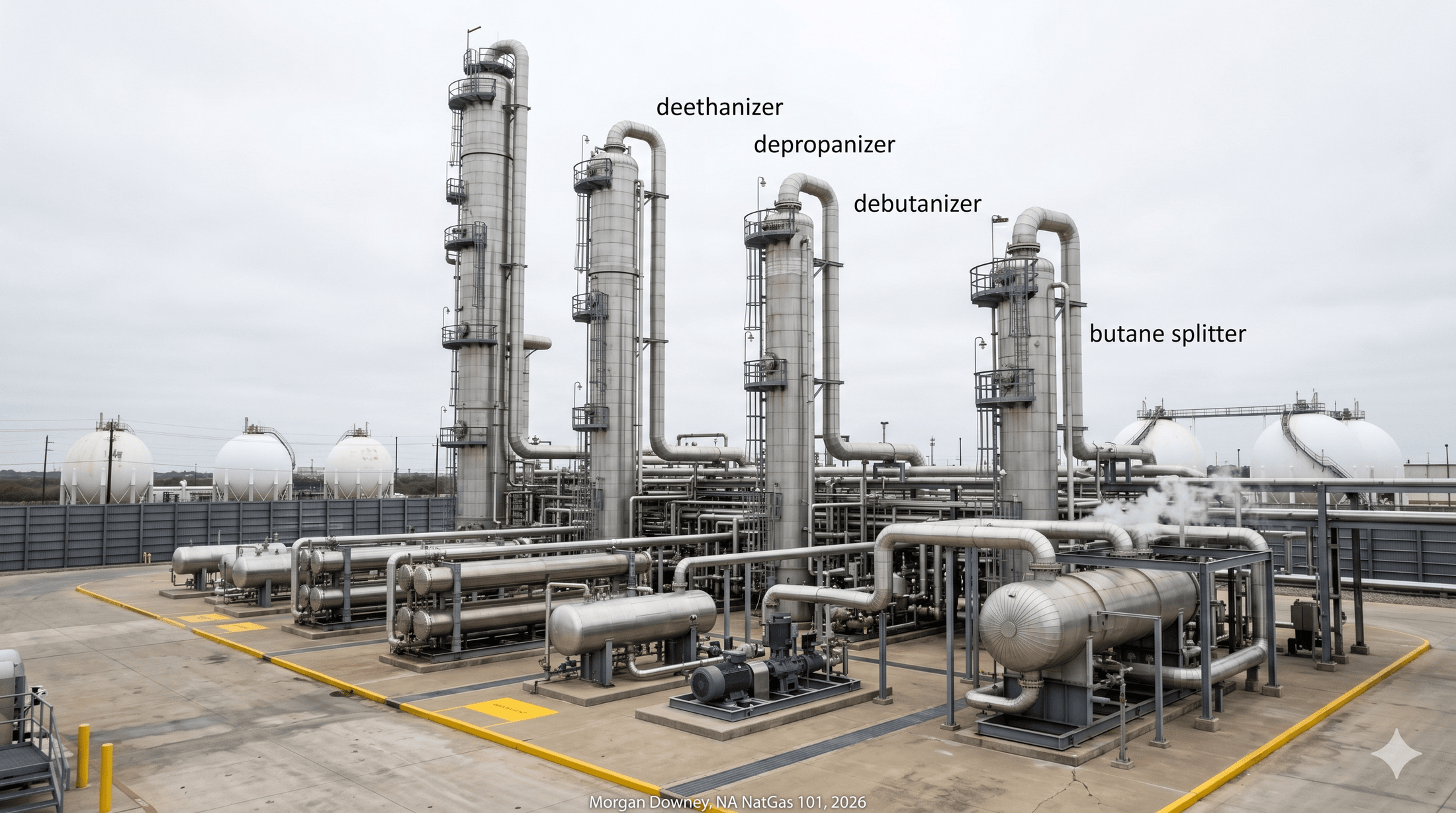

The fractionation train splits the Y-grade in sequence by boiling point. The deethanizer is the first column. Y-grade enters the column at intermediate pressure and ethane rises overhead as a purity-ethane product. Ethane is the dominant volume of the Y-grade, often 40 to 50 percent of the stream by volume, and its overhead recovery requires the largest of the columns in the train. The depropanizer is the second column. The deethanizer bottoms feed in, propane rises overhead as HD-5 propane meeting the GPA Midstream HD-5 specification, and the bottoms continue to the next column. The debutanizer is the third column. Mixed butanes rise overhead, the bottoms are pentanes-plus or natural gasoline that goes to a pentanes-plus storage tank or to a gasoline-blending terminal. The butane splitter is the fourth column. Mixed butane enters, normal butane and isobutane separate by their small boiling-point difference, and each leaves as a separate purity product.

The five purity products and their dominant end uses:

- Ethane: feedstock to Gulf Coast steam crackers that produce ethylene, the largest-volume petrochemical building block. The Gulf Coast cracker complex stretches from Corpus Christi through Houston to the Lake Charles area in Louisiana. Ethane export by ship from Morgan’s Point and Marcus Hook supplies international crackers, primarily in northwest Europe and India.

- Propane: HD-5 specification propane goes to the LPG market for residential heating, crop drying, transportation fuel, and petrochemical feedstock. Propane dehydrogenation, called PDH, converts propane to propylene at units in the Houston cluster and on the upper Texas coast.

- Normal butane: gasoline blending in winter months when Reid Vapor Pressure specifications allow, butadiene production via steam-cracking, and isomerization feedstock.

- Isobutane: alkylation feedstock at refineries for high-octane gasoline blendstock production. The legacy MTBE manufacturing demand collapsed in the early 2000s as US oxygenate regulation moved away from MTBE toward ethanol.

- Natural gasoline: gasoline blending for octane and vapor pressure adjustment, and diluent for Western Canadian heavy oil and bitumen blends pipelined to US Gulf Coast and Midwest refineries.

Each purity product trades on its own forward curve. Mont Belvieu propane trades against the OPIS Mont Belvieu propane assessment. Ethane trades against the OPIS Mont Belvieu purity ethane assessment. The five-product price stack is the basis for processing-plant economics across the entire US midstream segment. The chemistry that turned the wellhead stream into five separately priced commodities is settled. The price discovery happens at Mont Belvieu.

Residue Gas and Pipeline-Quality Compliance

The dry methane stream that leaves the demethanizer overhead is the residue gas. After the NGLs are stripped, the residue’s heating value moves much closer to pure methane. A typical residue gas leaves the plant at 1,000 to 1,030 Btu per standard cubic foot, against the 1,100 to 1,300 Btu of the wet inlet stream that fed the plant. The composition is roughly 95 to 99 percent methane with the balance distributed across nitrogen, residual ethane that the demethanizer left in the overhead, carbon dioxide that the amine unit did not strip to zero, and trace components.

The residue must meet the receiving pipeline’s tariff specifications. Each interstate pipeline files a tariff with the Federal Energy Regulatory Commission that defines the gas specifications under which the pipeline will accept gas at any receipt point. The specifications cover heating value (typically 950 to 1,100 Btu per standard cubic foot range, with operator-specific variation), water content (typically 7 pounds per million standard cubic feet), hydrogen sulfide (typically 4 ppmv, with some pipelines at 0.25 grains per 100 cubic feet), total sulfur (typically 5 to 20 grains per 100 cubic feet), carbon dioxide (typically 2 to 3 percent), oxygen (typically below 0.4 percent), and several other parameters covered in Chapter 5. The processing plant operator monitors the residue stream continuously through gas chromatography and online moisture analyzers and contracts with the pipeline operator to deliver gas within spec or accept the gas being rejected at the receipt meter.

The processing intensity required to meet specification is set by the inlet composition. Plants in the Marcellus dry-gas core need only modest processing because the inlet is already 96 to 98 percent methane and the impurities are minor. Many Marcellus dry-gas wells flow gas that meets pipeline spec on heating value and contaminants without any cryogenic NGL recovery; these wells go through a smaller dehydration-and-treating skid rather than a full processing plant. The economic threshold for cryogenic processing is the value of the C2-plus stream that can be recovered, weighed against the capital and operating cost of the cryo plant. When the frac spread is wide, recovery is profitable and even modestly wet streams move through cryo plants. When the frac spread is narrow, ethane recovery is sometimes rejected and the ethane is left in the residue stream as heating-value contribution rather than separated as a purity product. This decision, called ethane rejection, can shift the volume of US ethane production by 200,000 to 400,000 barrels per day depending on price conditions and processing-plant flexibility.

Plants in the Marcellus wet core, the Permian, the Eagle Ford condensate window, and the Bakken run heavier processing because the inlet stream carries 15 to 30 percent C2-plus and the residue cannot meet pipeline spec without separation. The cryogenic recovery is mandatory in those basins, not optional. The economics of the wet portion of the play depend on the cryo plant being available and on the NGL pipeline downstream having capacity to take the recovered Y-grade.

Plant Economics and Contract Structures

The midstream segment makes money by charging the producer a fee for gathering, processing, and fractionation, or by taking a share of the gas and the NGLs as in-kind compensation. Three contract structures dominate.

A fixed-fee contract pays the midstream operator a per-Mcf fee for gathering and processing and a per-gallon fee for fractionation. The midstream operator takes no commodity exposure. The producer keeps all of the residue-gas value and all of the NGL value, paid net of the fee. Fixed-fee contracts have become the default for modern shale acreage signed after 2015, partly because the midstream segment’s lenders and equity investors prefer the visible cash flow and partly because the producers prefer to retain commodity exposure they can hedge in liquid futures markets. Fixed-fee gathering and processing fees in the Marcellus and Permian core typically run $0.30 to $0.70 per Mcf for gathering and processing combined, with an additional $0.04 to $0.07 per gallon for fractionation.

A percent-of-proceeds contract, called POP, pays the midstream operator a percentage of the residue gas and NGL revenue. The midstream operator keeps a share of the value the plant produces; the producer keeps the balance. POP contracts align producer and midstream incentives because both parties benefit when commodity prices rise and both lose when prices fall. POP contracts dominated US gathering and processing in the 1980s and 1990s, persist on legacy acreage in the Mid-Continent and the Rockies, and are uncommon on modern Marcellus, Haynesville, and Permian acreage.

A keep-whole contract pays the midstream operator the gas-equivalent value of the NGLs it strips out, with the midstream operator keeping the NGLs themselves. The producer is paid as if the gas had been delivered as wet gas at its full heating value, regardless of whether the NGLs are stripped or left in. The midstream operator captures the difference between the NGL price and the gas-equivalent value. Keep-whole contracts are profitable to midstream when NGL prices are high relative to gas, and unprofitable when the opposite holds. The 2008 oil-price spike to $147 per barrel pulled NGL prices above gas-equivalent value by a wide margin and rewarded keep-whole midstream operators handsomely; the 2015 to 2016 commodity collapse compressed the spread and pushed several keep-whole operators to renegotiate contracts to fixed-fee terms or to take on operating losses on the unprofitable plants.

The frac spread is the per-MMBtu margin between Mont Belvieu NGL prices and Henry Hub gas prices, weighted by typical Y-grade composition. CME Group lists futures contracts on a standardized OPIS-based frac spread, and the EIA publishes a weekly frac-spread series in its Natural Gas Weekly. A wide frac spread makes processing profitable and makes wet-gas wells attractive to producers because the NGL barrel value exceeds the gas-equivalent value by a meaningful margin. A narrow frac spread does the opposite. The frac spread spent most of 2008 through 2014 wide on high oil prices, narrowed sharply during the 2015 to 2016 collapse, recovered through 2018 to 2019, narrowed again during the spring 2020 demand collapse, and traded in a moderate range through 2024. The capital allocation decisions of every wet-gas producer in North America are conditioned on the forward frac spread.

The midstream operator’s profit per Mcf processed is small in absolute terms. A Permian processing plant earning $0.45 per Mcf in fixed-fee gathering, processing, and treating runs on margins that are highly sensitive to throughput. A 200 MMcf/d plant operating at 95 percent of capacity earns $31 million per year in fees on the gas alone, before fractionation, and the unit’s break-even occupancy depends on how much capital was sunk in the build. The midstream segment is a volume business with thin per-unit margins and high asset-specificity. The plants do not move. The contracts that fill them do.

Geography of US Gas Processing

The processing footprint follows the production footprint with a lag. New gathering systems and processing plants typically lag wellhead production by 6 to 24 months because the construction timeline for a 200 MMcf/d cryogenic plant runs 12 to 18 months from groundbreaking to first gas, and the FERC and state permits that precede groundbreaking add another 6 to 12 months. The lag is the structural reason that fast-growing basins routinely run into processing-capacity bottlenecks before the new plants come online.

Mont Belvieu and the Texas Gulf Coast hold the dominant share of fractionation. Beyond Mont Belvieu, the Houston Ship Channel cluster, the Beaumont and Port Arthur cluster, and the Lake Charles cluster in Louisiana operate fractionation, ethane export, and propane export facilities. The Marcus Hook complex on the Delaware River outside Philadelphia operates fractionation and export capacity built on top of the former Sunoco refinery and is the principal Northeast outlet for Marcellus and Utica Y-grade.

The Marcellus and Utica processing footprint clusters in the Appalachian wet core. Southwestern Pennsylvania (Washington, Greene, and Westmoreland counties), the West Virginia northern panhandle (Marshall and Wetzel counties), and eastern Ohio (Belmont, Monroe, and Harrison counties) hold the majority of Appalachian processing capacity. MPLX (formerly MarkWest) operates the largest single position, with major plants at Houston and Sherwood in West Virginia, the Cadiz complex in eastern Ohio, and additional capacity in southwestern Pennsylvania. Williams operates the Oak Grove complex in West Virginia. Energy Transfer operates several plants and the Mariner gathering and NGL pipeline system. EQT and other large producers run integrated gathering operations on parts of their acreage.

Permian processing clusters around the Delaware sub-basin in southeast New Mexico and west Texas (Eddy, Lea, Loving, Reeves, and Culberson counties) and the Midland sub-basin in west Texas (Midland, Martin, Howard, and Glasscock counties). Targa Resources operates the largest Permian gathering and processing position, with plants at Carlsbad, Pecos, and across the Midland sub-basin. Enterprise, Energy Transfer, and MPLX round out the Permian processing build. The pace of Permian plant construction through 2017 to 2024 was the structural cause of the recurring Waha negative-pricing episodes covered in Chapter 8: gathering and processing capacity could not be permitted, financed, and built fast enough to absorb the associated-gas growth coming off the oil rigs.

Bakken processing capacity sits in McKenzie and Williams counties, North Dakota. ONEOK operates the largest position. The Bakken’s gathering and processing problem in the early 2010s was acute because the producers were drilling oil wells and the gas volumes outran both processing capacity and pipeline takeaway. North Dakota’s flaring share of total gas production exceeded 35 percent at the 2014 peak before regulatory limits and incremental midstream investment pulled the share back below 10 percent by the late 2010s.

The Conway hub in central Kansas is the secondary fractionation center, primarily serving the Mid-Continent producing basins (Oklahoma’s STACK and SCOOP plays, the Hugoton, the Anadarko basin) and the Rocky Mountain plays (Piceance, DJ, Powder River) through ONEOK’s Bakken NGL Pipeline and the Mid-Continent gathering systems. Conway capacity is a fraction of Mont Belvieu and the price discovery is thinner, but the hub remains the relevant inland alternative for producers whose Y-grade is uneconomic to ship to the Texas Gulf Coast.

Major Midstream Operators

The midstream segment is consolidated. Six or seven companies run most of the gathering, processing, and fractionation capacity in the United States.

Enterprise Products Partners is the largest pure-play midstream operator, with the broadest position across NGL pipelines, fractionation at Mont Belvieu, ethane export from Morgan’s Point, and crude and refined-product logistics. The partnership has run consistently for two decades and remains the price-discovery and infrastructure anchor of the US NGL market.

Williams Companies operates long-haul gas pipelines (most prominently Transco, the largest US interstate gas pipeline by throughput) along with extensive Northeast and Marcellus gathering and processing through its Williams Field Services and Northwest Pipeline subsidiaries.

Energy Transfer is the most diversified large midstream operator, with major positions in NGL pipelines, gas pipelines, gathering and processing across multiple basins, refined-product pipelines (the Sunoco Logistics legacy), and crude pipelines. Energy Transfer is structured as a master limited partnership and the family of related Energy Transfer entities reflects a long history of acquisition and consolidation.

ONEOK runs the dominant NGL pipeline and fractionation footprint at Conway, and operates Bakken NGL gathering and a long Bakken-to-Mid-Continent NGL pipeline system. ONEOK acquired Magellan Midstream Partners in 2023 in a deal that combined NGL and refined-product logistics under a single operator.

Targa Resources runs the largest Permian gathering and processing footprint, with plants across the Delaware and Midland sub-basins, NGL pipeline takeaway to the Texas Gulf Coast through its Grand Prix system, and fractionation and propane export at Galena Park.

MPLX is Marathon Petroleum’s midstream subsidiary, formed in 2012 and expanded through the 2015 acquisition of MarkWest Energy Partners that gave MPLX its Marcellus and Utica processing footprint. MPLX operates major Marcellus and Utica gathering and processing along with Permian gathering, refined-product logistics, and crude pipelines.

Kinder Morgan operates long-haul gas pipelines (including the Tennessee Gas Pipeline and the El Paso Natural Gas system), refined-product pipelines, and crude pipelines, with limited gathering and processing exposure relative to the integrated peers above. DCP Midstream was acquired by Phillips 66 in 2023 and integrated into the Phillips 66 midstream segment, which folded the legacy DCP gathering, processing, and fractionation footprint under the Phillips 66 corporate structure.

The pace of consolidation through the 2010s and 2020s reflects the capital intensity of the segment, the scale efficiencies on shared interconnect infrastructure, and the lower cost of capital available to the largest midstream balance sheets. The segment is unlikely to consolidate further at the very top end. The mid-tier operators continue to be acquired into the top six.

MarkWest’s Marcellus Build, 2008-2015

MarkWest Energy Partners was a small Denver-based midstream MLP with a footprint in the Mid-Continent and a single Appalachian asset, the Kenova fractionator in West Virginia, when the Marcellus shale began to produce wet gas in earnest in 2009. Range Resources had drilled the Renz 1 in southwestern Pennsylvania in 2004, established the Marcellus as a viable shale play through 2007 to 2008, and needed gathering and processing capacity to commercialize the wet portion of its acreage. MarkWest signed gathering and processing contracts with Range and built the first Houston processing plant in Pennsylvania (the Washington County plant, not the Texas city) starting in 2009.

The build accelerated. By 2014 MarkWest had constructed processing capacity at Houston, Mobley, and Sherwood (in West Virginia), Cadiz (in eastern Ohio), and several smaller satellite plants, totaling over four billion cubic feet per day of gathering and processing capacity across the Marcellus and Utica wet cores. The build was financed by a series of MLP equity issuances, project-level debt, and joint ventures with infrastructure investors. MarkWest’s market capitalization grew from a few hundred million dollars in 2008 to over fifteen billion at the time of the 2015 sale to Marathon Petroleum’s MPLX subsidiary.

The MPLX acquisition closed in late 2015. MarkWest became MPLX’s Marcellus and Utica gathering and processing platform, and the assets remain the largest single midstream position in Appalachia today. The Range Resources contracts that anchored the original Houston plant in 2009 are still flowing gas through MPLX’s Houston complex sixteen years later.

The residue gas leaves the plant at the receipt meter on an interstate pipeline. Chapter 10 follows the gas down the long-haul pipe, through the compressor stations that move it across continents, to the city gate where the local distribution company takes delivery.